Apple (NASDAQ: AAPL) has been one of the best-performing stocks of the past decade. But 2022 has been a rough year, as the iPhone maker has seen its stock price decline by 30%. Even so, its charts may not necessarily indicate a buying opportunity.

Screening the numbers

Apple is renowned for selling its flagship products. But aside from hardware, the firm also sells services. These include commissions from app store sales and revenue from its cloud service.

| Business segment | Revenue (FY22) | Gross margin (FY22) |

|---|---|---|

| Products | $316.20bn | 36.3% |

| Services | $78.13bn | 70.5% |

| Overall | $394.33bn | 43.3% |

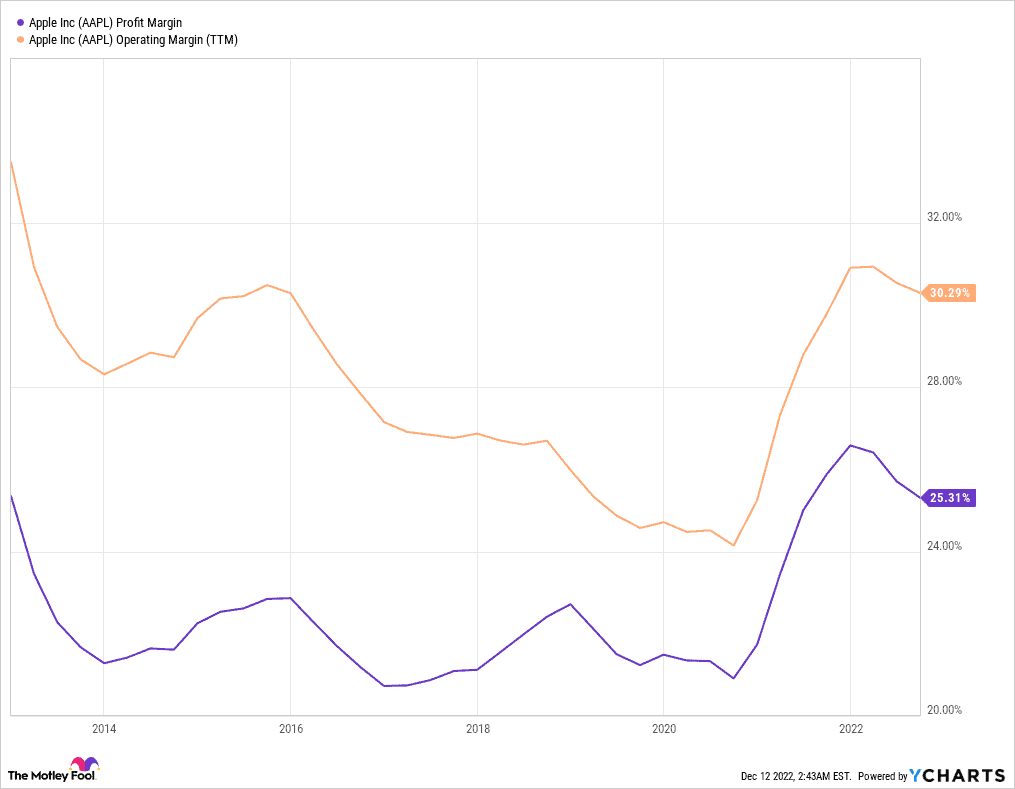

The two segments have drastically different margins. But all together, the group’s operating and profit margins are considered to be healthy at above 25%. More importantly, these margins have held up rather steadily over the last decade.

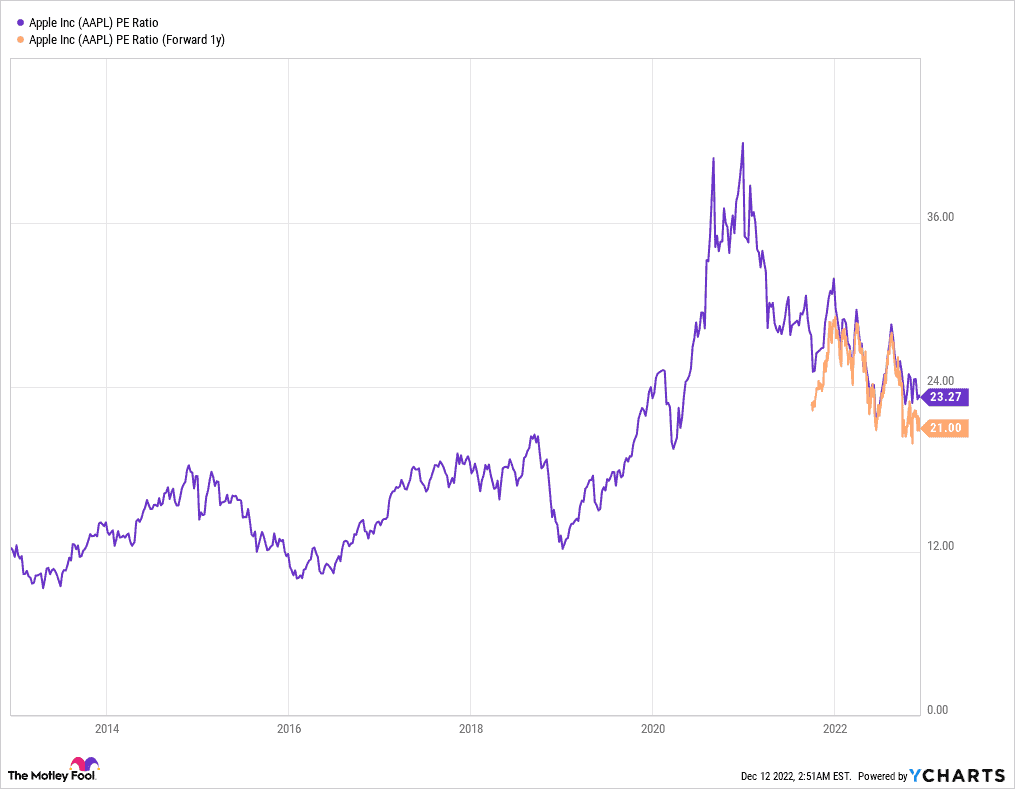

Nonetheless, the stock currently trades at a price-to-earnings (P/E) ratio of 23 and a forward P/E of 21. This is slightly more expensive than the S&P 500‘s average P/E of 21, which could indicate that Apple stock could be on the pricier side. The tech stock’s price-to-earnings (PEG) ratio isn’t particularly cheap either at 2.7, which is above the desired level of 1.

Lack of stock

It’s worth noting, however, that the ‘elevated’ levels of P/E can be attributed to the current and expected decline in earnings. This is due to problems with Apple’s biggest iPhone manufacturer, Foxconn.

Besides the constant shutdowns in China relating to COVID, workers have also been clamouring for better pay and working conditions. But due to complaints falling on deaf ears, protests have erupted. This has impacted iPhone production volumes substantially, as its facilities are now only operating at a 30%-40% capacity.

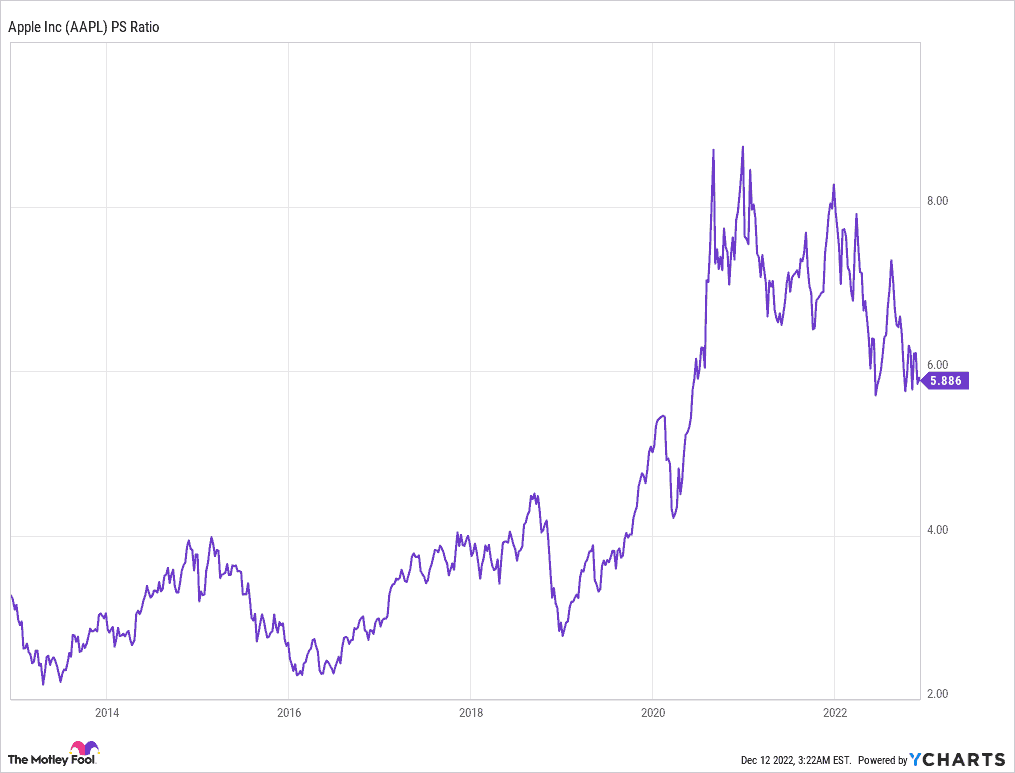

Consequently, this has seen the California-based company’s price-to-sales (P/S) ratio remain at elevated levels. Nevertheless, Apple is looking to mitigate its supply chain issues by branching out of China to other countries like India and Vietnam.

Fruitful returns

Therefore, the conglomerate’s multiples are inevitably going to suffer as these indicators only take a short-term outlook into account. However, its long-term prospects could be brighter if it manages to diversify its production risks.

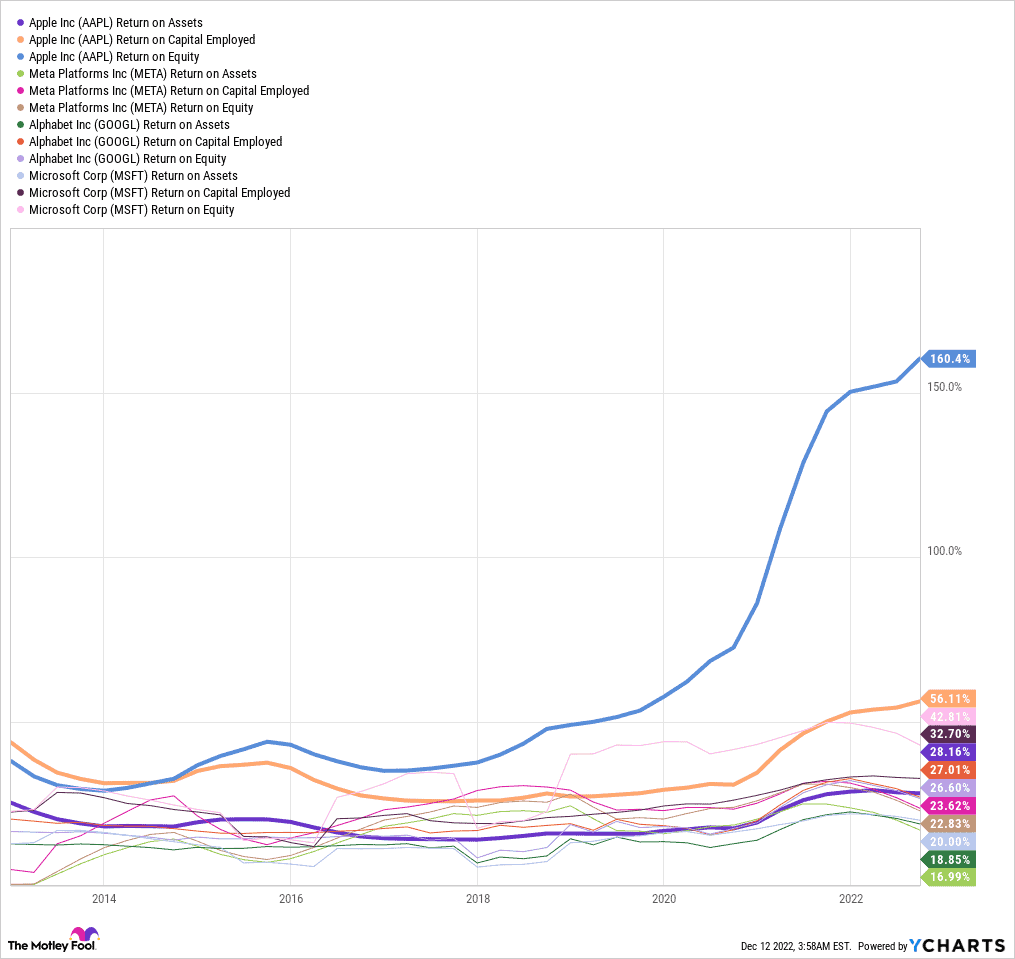

After all, despite its current overvalued metrics, there’s no shying away from the manufacturer’s excellent returns over the past decade. In fact, when compared to its big tech peers, Apple has consistently outperformed and grown its return on capital employed, equity and assets. This indicates that the group is capable of producing excellent shareholder returns, and is probably why it’s one of Warren Buffett’s biggest holdings.

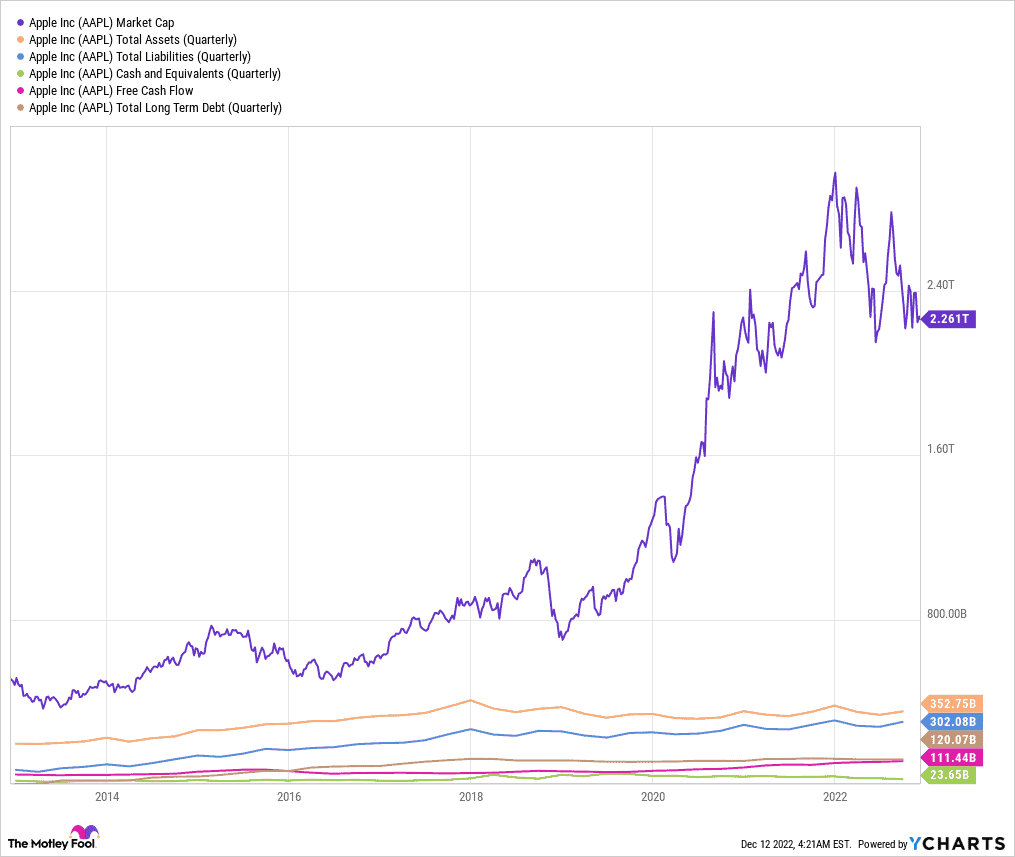

That being said, the state of the firm’s balance sheet is something worth noting. A high debt-to-equity ratio isn’t ideal, especially when its net debt stands at $71.77bn. But given the tech giant’s healthy free cash flow and cash and equivalents, it should be able to pay it off without too much of a hassle. Additionally, its net debt only constitutes about 2% of its total market cap. This means that Apple can easily raise more capital to pay off its debt without diluting shareholders too heavily.

So, is Apple stock considered cheap? Well, given its current multiples and short-term outlook, no. However, analysts still rate the stock a ‘strong buy’ with an average price target of $180. Having said that, supply chain fears, a substandard balance sheet, and a slowdown in product innovation makes me wary. Therefore, I’ll be looking to invest in other shares in the meantime.