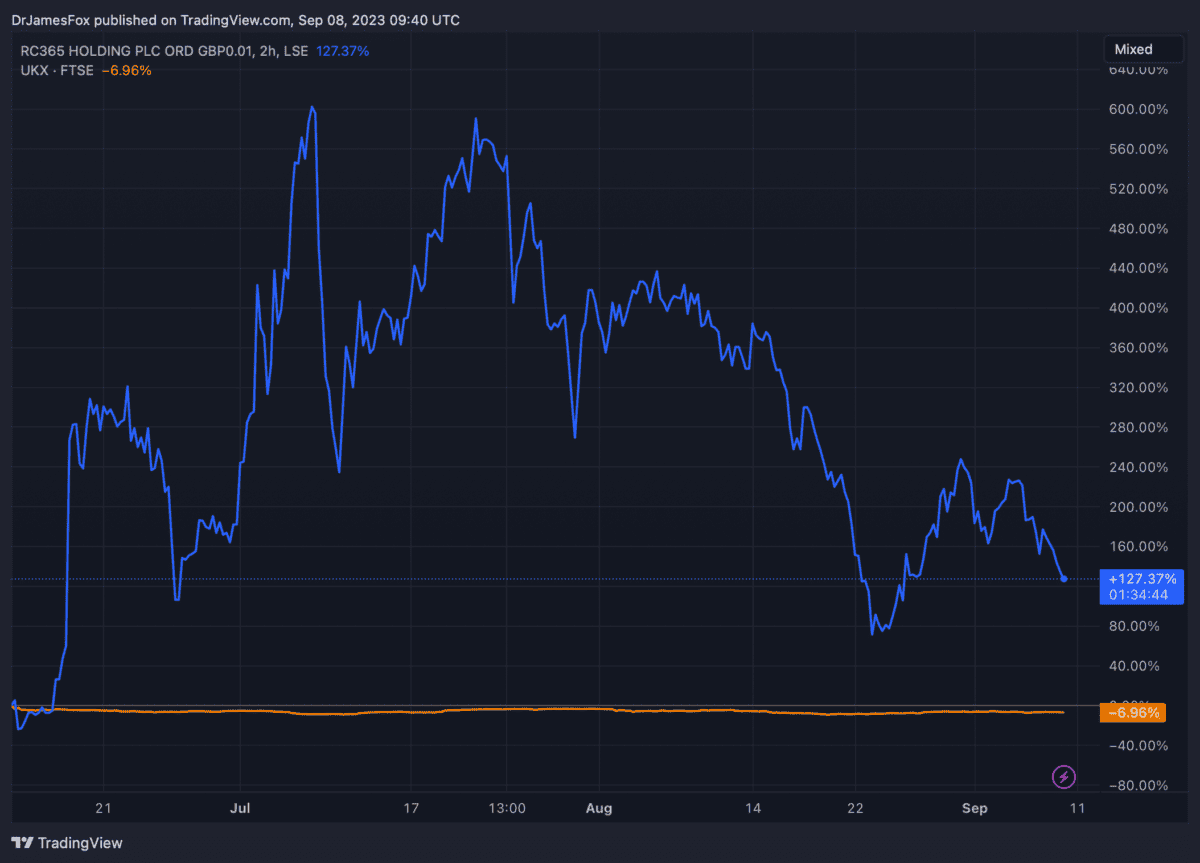

RC365 (LSE:RCGH) shares have given back more than half of their gains. But the stock is still up 170% over 12 months. It remains one of the best performing UK-listed companies. So it is worth considering for a portfolio?

The chart below highlights how the Asian tech firm has outpaced the FTSE 100.

How to value RC365

Valuing a company like RC365, which isn’t currently profitable, requires alternative metrics since the traditional price-to-earnings (P/E) ratio isn’t applicable.

One common approach is to assess the company’s potential based on its growth prospects, such as its revenue growth rate or user base expansion.

This method evaluates the company’s ability to capture market share and generate future revenue streams, which can be particularly relevant for growth-oriented stocks like RC365.

Another valuable approach is to examine the company’s relative valuation within its industry or sector. This involves comparing RC365’s key metrics, such as revenue multiples or growth rates, to those of its competitors or peers.

By assessing how RC365 stacks up against similar businesses in terms of market positioning and performance, we can gain insights into its relative value within the industry, even in the absence of profitability.

Relative valuations

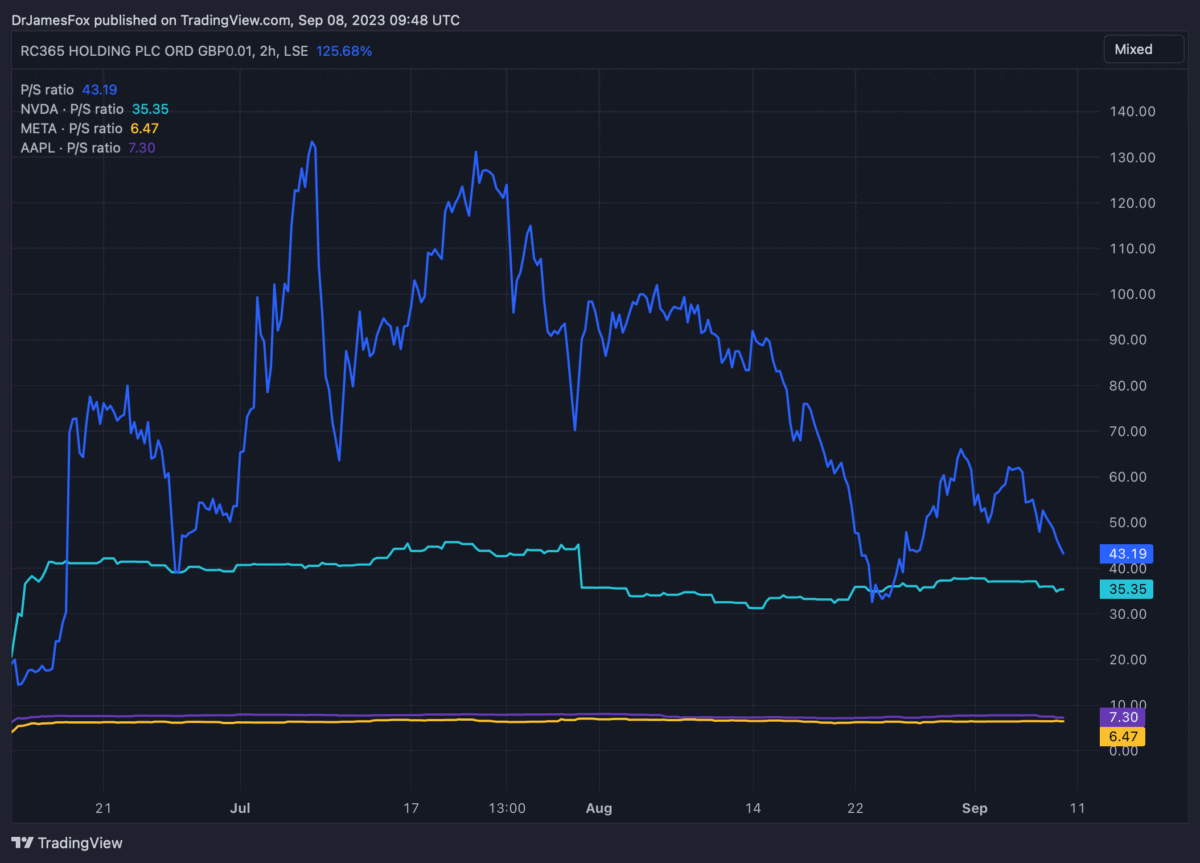

RC365’s valuation appears notably high, with the Hong Kong-based company currently trading at a staggering 43 times its revenue. This valuation level places it among the most expensive stocks in the market.

To put it into perspective, a price-to-revenue ratio of 10 is typically deemed quite expensive, underscoring the considerable premium attached to RC365’s shares.

The chart below shows its P/S (same as price-to-revenue) ratio versus major companies companies including Meta, Alphabet, and Nvidia.

On a trailing 12-month basis, it’s worth recognising that Nvidia is also considered expensive. However, with the AI boom, profits are soaring and the medium-term forecast is very strong.

Growth prospects

Unfortunately, there’s very little to substantiate the huge share price growth we’ve seen this year. The stock appears to have risen on the back on speculation concerning a MoU about AI.

And this was followed by an article titled ‘Missed Nvidia? This London-based AI stock has the potential to achieve a remarkable surge of over 1,000%‘.

When we look at performance, RC365 is clearly a minnow of the publicly-listed world. The firm’s revenue double to HK$16.9m (£1.5m) in FY23, but remains negligible.

Meanwhile, losses increased significantly over the period, amounting to HK$5.4m (£530k), up from HK$3.9m in the previous year.

So is RC365 justifying the hype? I think not. It seems likely that the share price will continue falling, having peaked in July, perhaps reaching levels seen last year.

Looking at valuation metrics, fair value likely exists somewhere between 10p and 15p a share. That’s still considerably lower than where the stock sits today.

Of course, the company and the stock could perform well in the future. But it’s worth highlighting that CEO Chi Kit Law holds 69.75% of issued shares. If he elects to cash in on the elevated share price, the stock could tank.