If I’d invested £1,000 in Hargreaves Lansdown (LSE:HL.) a year ago, I’d now have £830 plus £45 in dividends — a disappointing return.

Despite sporadic upward movements, the stock is down 17% due to a challenging environment for private investors, marked by a cost-of-living crisis and heightened stock market volatility.

Moreover, Hargreaves — the UK’s top investment platform — has faced difficulties sustaining its pandemic-era growth amid the post-Covid economic reopening.

Problems arising

Hargreaves remains the UK’s largest brokerage by a country mile. It has an intuitive platform and excellent customer support — as a customer I can vouch for the latter.

However, its peers, including AJ Bell, are growing faster in terms of client volume. One of the fundamental reasons for this is Hargreaves’ fee structure. It’s more expensive than its peers with every trade costing between £5.95 and £11.95 depending on frequency.

That’s fine if I’m investing large amounts. But if I was looking to build a portfolio of smaller holdings or practice pound-cost-averaging (that is, drip-feeding my investments so the price averages out over time), this ‘premium pricing’ could be off-putting. Given the current climate, Hargreaves may need to make its pricing more appealing to avoid a slower pace of growth.

Of course, there are multiple ways of measuring growth. One is net new customers — this is where Hargreaves is floundering — while another is assets under administration.

In theory, investors with more money are more likely to be content with Hargreaves’s higher fees. And from a net interest margin perspective — brokerages lend out customers’ cash to the market — these high-wealth investors are much more valuable.

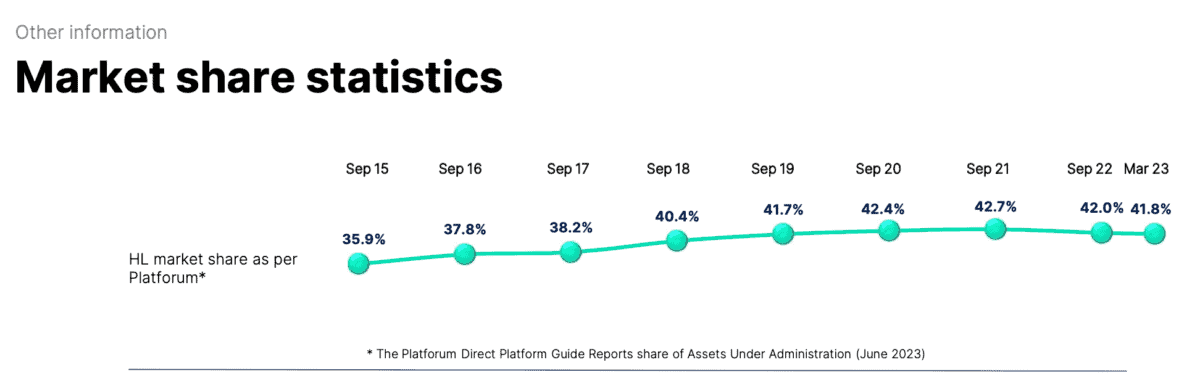

The below graph highlights that while the Bristol-based broker has lost some market share, it has a dominant position in the market.

Worth the risk

Early indications also suggest that Hargreaves could drop out of the FTSE 100 on Wednesday (29 November) after FTSE Russell, which manages the FTSE indexes, announced that the firm could be replaced as its market value falls.

Nonetheless, Hargreaves has attractive near-term valuation metrics compared to its peers, trading at just 10.3 times 2023 earnings.

However, as alluded to above, the problem is growth. The below table shows that Hargreaves isn’t forecast to deliver another bumper year like 2023 through the medium term. As such, the forward price-to-earnings ratio is more expensive, but remains much cheaper than its peers. It still looks undervalued to me.

| 2023 | 2024 | 2025 | 2026 | |

| EPS (p) | 68.3 | 60.4 | 58.8 | 63 |

| P/E | 10.3 | 11.7 | 12.1 | 11.2 |

Long story short, I still have faith in Hargreaves to continue growing. But I think it needs to make some changes. This could mean making its fees proportionate to the size of the trades, or having a monthly membership for fee-free dealing.

It’s also worth considering the case of Charles Schwab. It’s the biggest brokerage in the US and it makes all its income from net interest margins.

If Hargreaves were to do the same, it would lose fee income, but it could take an even more commanding position in the market, potentially leading to it having significantly more assets under administration.

I’d buy more of this stock, if I had the capital, despite slowing growth. It remains in pole position to dominate the sector, I feel.