The Diageo (LSE:DGE) share price continues to fall on Tuesday (4 January) as the company’s latest update is in. And it’s not hard to see why – results are uninspiring and the outlook is gloomy.

Volumes are down, costs are up, and the impact of tariffs is likely to make this worse. I’m planning to stay the course with this one, but I wouldn’t blame anyone else for cutting their losses and moving on.

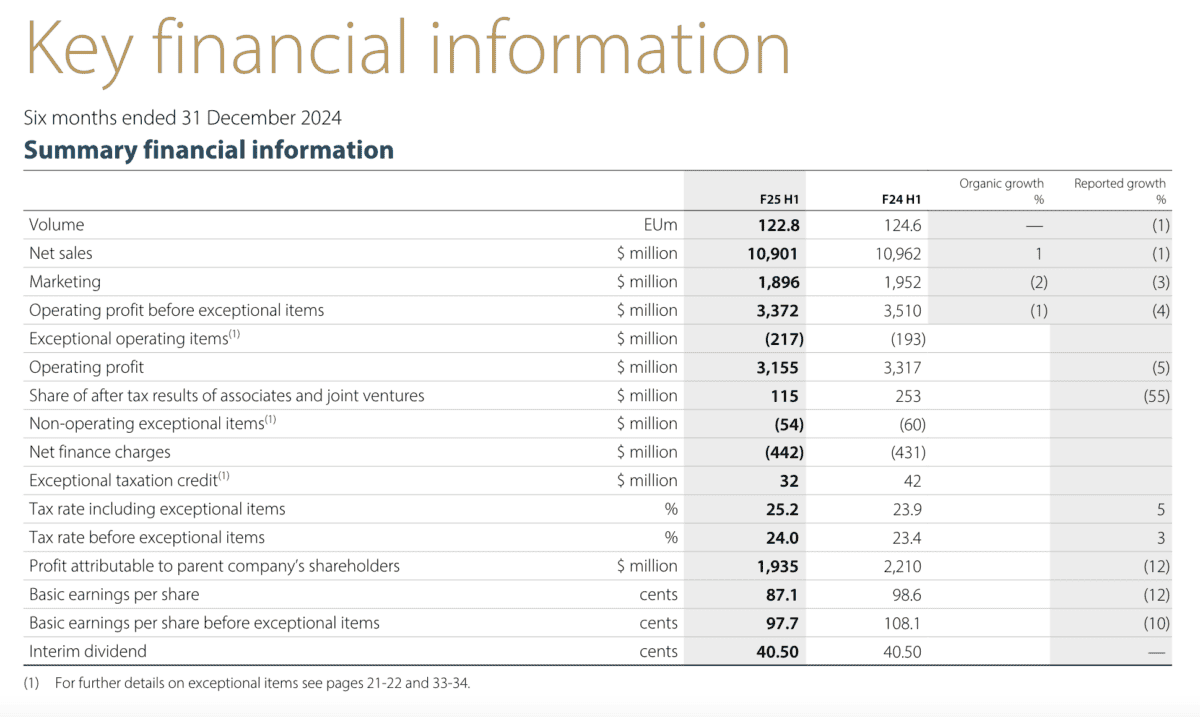

Return to growth?!

Debra Crew talked about the company’s return to growth, but investors have to look carefully to see what she’s talking about. The only reported number that’s higher than it was a year ago is tax.

Source: Diageo 2025 Interim Results

Revenues were down 1%, but this was the result of an unfavourable shift in foreign exchange results. Without this, sales actually increased 1% — so there we are, growth.

The trouble with this is it’s likely to be wiped out by just about any kind of inflation. Sure enough, continued overhead investments meant operating profits were down on the same basis.

On top of this, the firm’s balance sheet is becoming a concern. Increased borrowings over the last five years combined with falling profits mean Diageo’s leverage ratio is – by its own standards – too high.

Tariffs

The big reason the Diageo share price has been falling lately is the threat of tariffs from the US. And the latest results confirmed what everyone already knew – these are likely to be a problem.

The firm’s recent performance in the US has been driven by Crown Royal and Don Julio. One of these is made in Canada and the other is made in Mexico, which puts them right in tariff territory.

There isn’t really much of a way around this, so Diageo is going to have to try to tough it out. But the higher costs are likely to weigh on both sales and profits until something changes.

The firm is withdrawing its guidance for organic sales growth of between 5% and 7% over the medium term as a result of incoming tariffs. But I think investors should question how likely that was anyway.

Short-term problem?

Diageo’s problems just seem to keep coming, but they do look temporary. And the firm’s competitive advantages – the scale and the strength of its brand portfolio – are still intact.

On the subject of tariffs, Goldman Sachs has suggested these might not last as long as many are anticipating. In other words, they’re a negotiating tool. I think it might be right about this.

Furthermore, tequila has to be produced in Mexico (just as Scotch whisky has to be made in Scotland) so it’s not as though rivals have scope to cut into Diageo’s competitive position. That’s also important.

In the meantime, one number that isn’t down is the interim dividend, which is staying fixed. But over the long term, investors are going to need more than this to make the stock a good investment.

Foolish takeaways

In short, I think the long-term outlook for Diageo is still reasonably promising. But the big question is when the near-term challenges are going to subside.

Waiting brings an opportunity cost. So investors need to figure out how long they’re prepared to wait for what could ultimately be limited sales growth.