International Consolidated Airlines (LSE:IAG) shares have delivered a tasty return over the last year. Someone who invested £10k in the FTSE 100 business 12 months ago would have seen the value of their investment rise to £13,817.

They’d also have received dividends totalling roughly £147 in that time.

But IAG shares have been in a sharp descent in recent weeks, reflecting worries over the economic environment and mounting competition.

Can the British Airways owner rise once again? And should investors consider buying IAG shares for their portfolios?

US threats

Airlines are among the most cyclical companies out there. So it’s no surprise to see them falling sharply in value as intensifying trade wars have darkened an already fragile outlook for the global economy.

In December, The International Air Transport Association (IATA) had predicted revenues and passenger numbers above $1trn and 5bn respectively for the first time in 2025. Now those forecasts are looking shaky, and particularly so as recessionary risks mount in the US, the industry’s most profitable market.

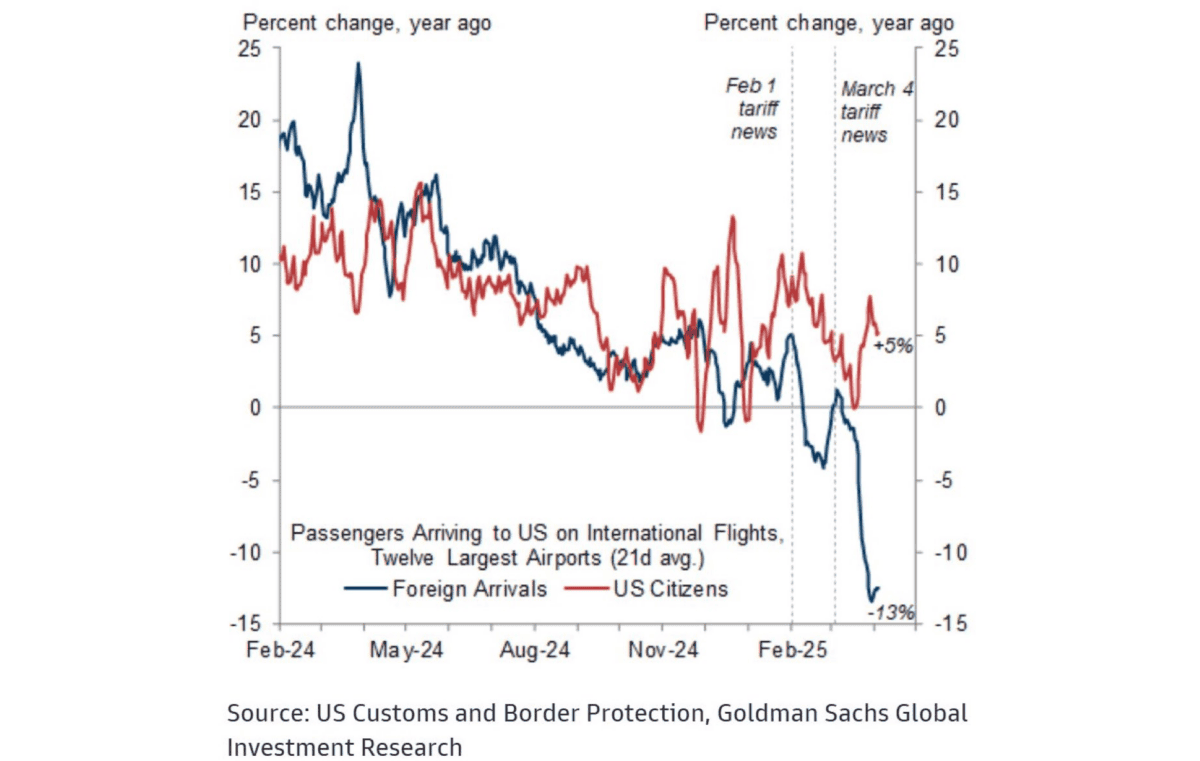

IAG, which has significant exposure to the US through its British Airways, Iberia, Level and Aer Lingus brands, would be especially vulnerable to a US downturn. Just under a third of the company’s air capacity is allocated to its Stateside routes.

There’s a good chance IAG’s already witnessing weakening transatlantic demand. Tigher immigration rules, and widescale criticism of the controversial Trump presidency, are leading to reduced bookings on US-bound flights across the industry:

Other challenges

Other significant obstacles for IAG and its share price are more traditional. Industry competition remains a substantial threat to revenues and airlines’ profit margins.

This danger took on added significance for the FTSE 100 firm in March too, as it agreed to concessions on lucrative routes to and from Boston, Miami and Chicago. IAG’s British Airways, Aer Lingus and Iberia plan to surrender London airport slots aims to soothe concerns of the UK competition watchdog.

Finally, company profits are vulnerable to travel infrastructure problems over which they have no control. Strikes by airport staff have long been a problem across IAG’s routes. Power outages at Heathrow — and subsequent flight cancellations said to have cost airlines up to £100m — have been a more recent hazard.

Risk vs reward

Yet investing in IAG shares also comes with some opportunities. The global commercial aviation market is tipped to grow substantially over the long term, driven by booming emerging markets. And heavyweight brands like British Airways give the Footsie company a great chance to exploit this.

Airbus also forecasts global air traffic will more than double over the next 20 years.

Yet on balance, I still believe IAG shares carry too much risk, even at current prices. The company now trades on a price-to-earnings (P/E) ratio of 4.2 times, which I think fairly reflects the huge challenges it faces.

There’s no shortage of cheap quality shares to buy following recent market volatility. So I think investors should consider adding other shares to their portfolios.