BT‘s (LSE:BT.A) shares have enjoyed robust gains over the last 12 months. Yet things aren’t quite as cheery when analysing the telecoms giant’s performance over the longer term.

At 174.7p per share, BT’s share price is down 60.9% from the 446.7p it was trading at 10 years ago. This means that £10,000 invested in the FTSE 100 company back then would now be worth roughly £3,911.

In better news, the stock’s long-term investors have received a steady stream of dividends in that time. These have totalled 99.12p per share, which means the total return on a £10k investment would be £6,131, or -38.7%.

But past performance isn’t always a reliable guide to the future. With the business steadily slashing costs — it’s targeted total savings of £3bn by 2029 — and spending on its colossal broadband rollout programme moderating, things could be looking brighter for the company.

So could BT be about to rebound? And should investors consider buying its shares this June?

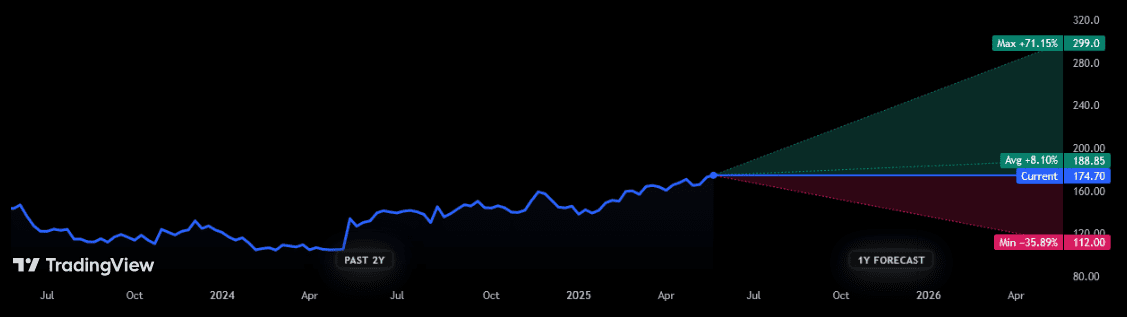

Where are prices heading next?

Price forecasts for BT shares aren’t available over a long-term horizon like a decade. But City analysts have laid down their projections for the next 12 months.

Unfortunately they’re not as instructive as investors may have hoped. The average price estimate among the 13 brokers rating BT stock believe it will rise by high single digits over the next year.

However, individual forecasts vary substantially. One especially bullish analyst thinks BT could rise almost three-quarters in value during the period. Conversely, the most pessimistic broker reckons they could drop by almost a third.

Could valuations provide a clue?

As I say, BT’s share price has climbed substantially over the last year (up 36.3%). As a consequence, it doesn’t look like the bargain it was last June. And this could prove a barrier to the company hitting those bullish price estimates.

The company now trades on a forward price-to-earnings (P/E) ratio of 9.8 times. This is above the figure of 6.7 times it carried this time last year. Furthermore, it’s slightly ahead of the 8.9 times it’s averaged over the last 10 years.

BT shares also offer less value from a passive income perspective. Its forward dividend yield was 6.1% a year ago, and has averaged 5.5% over the last decade,

Today, the dividend yield sits at 4.7%.

So what’s next?

On balance, I’m not convinced BT can continue its recent share price recovery. In fact, it’s a share I wouldn’t go near right now.

Telecoms companies play a critical role in the booming digital economy. The problem is that competition in the broadband and mobile markets is fierce, and BT’s sales performance keeps on disappointing.

In the 12 months to March group adjusted revenues declined 2% year on year to £20.4bn. Sales at its Consumer division dipped 1% and Business turnover dropped 4%.

The sky-high levels of debt the company carries is another major concern to me. Net debt keeps on rising and was £19.8bn as of March, up 2% year on year.

Given BT’s huge capital expenditure bills and large contributions it’s making to soothe the pension scheme deficit, I’m expecting its balance sheet to remain under severe pressure.

On balance, I think investors should consider buying more robust UK shares this month.