A Self-Invested Personal Pension (SIPP) allows parents or guardians to start saving for a child’s retirement decades in advance.

Contributions of up to £2,880 a year attract 20% tax relief from the government, turning it into £3,600. This is the case even if the child has no income.

With compounding returns over 50 or 60 years, even modest monthly investments could grow into a substantial sum.

While the money can’t be accessed until retirement age, that’s also the beauty of it. The long time horizon means growth potential is enormous.

For parents thinking long term, a junior SIPP could be one of the smartest, most tax-efficient gifts to give a child’s future self.

A parent or grandparent may want to use this to complement the Junior ISA. The ISA can be accessed by the child at the age of 18.

If the Junior ISA (maximum contributions of £9,000 per annum) and SIPP are fully allocated for the year, a bare trust could be the next consideration.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

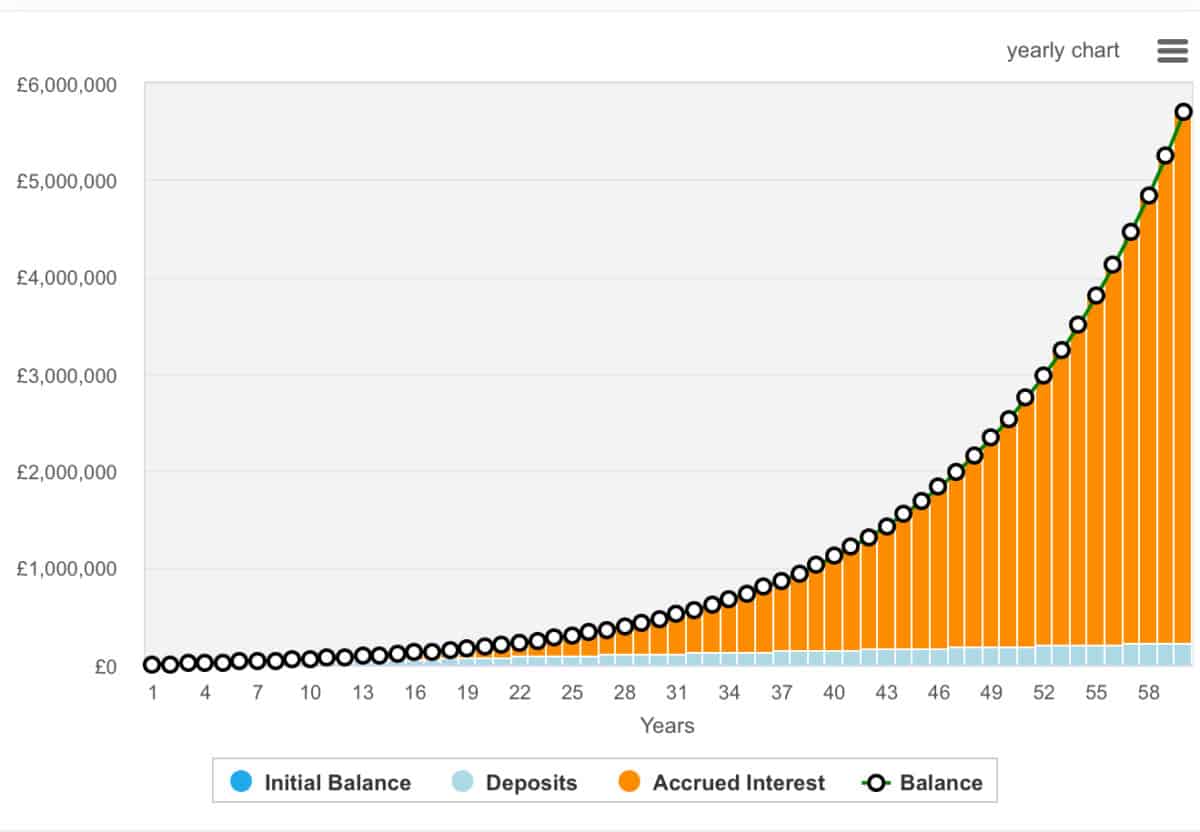

Running the maths

Imagine starting a SIPP from birth and contributing £320 a month including the tax relief.

For the sake of this calculation, I’m going to assume the child, on becoming an adult, continues to contribute £320 — even though inflation will make this a very small figure by the end of the period.

So, after 60 years of compounding at 8% annually — a very achievable figure based on historic market performance — the SIPP would be worth £5.7m.

Now, remember, only £230,000 of this would have come from contributions. The rest is all interest on interest — that’s compounding.

Where to invest?

With a SIPP, and something that’s going to be invested for such a long time, my preference is to invest in trusts, funds, and conglomerates.

For example, my daughter’s ISA doesn’t have dealing fees and is around eight times larger than her SIPP, which does have dealing fees — because we use Hargreaves Lansdown.

It’s a practical decision.

One investment that I have in her portfolio and believe is worth considering is Scottish Mortgage Investment Trust (LSE:SMT).

Managed by Tom Slater and Lawrence Burns, the trust focuses on transformative, high-growth companies — both public and private — that have the potential to multiply in value over time.

Its portfolio includes innovators such as SpaceX, ByteDance, and MercadoLibre, alongside listed giants like Amazon and Meta.

However, investors should remember that Scottish Mortgage’s performance can be volatile.

The investment trust uses gearing (borrowing to invest), which amplifies both gains and losses.

This proved painful in 2021–22, when growth stocks sold off sharply.

Today, though, the shares trade at roughly a 12% discount to net asset value (NAV), suggesting continued value for money and some caution.

For long-term investors, that discount could represent an attractive entry point.

While risks remain — particularly from rising rates and private market valuations — the trust’s patient, conviction-led approach gives it unique exposure to global innovation.