At the start of 2025, the Aston Martin (LSE:AML) share price wasn’t in great shape at 106p. Now at 59p as we move towards 2026, it’s in a complete mess.

This means the FTSE 250 stock is down 98% since early 2019!

Yet Rolls-Royce serves as a reminder of what can happen if an iconic British company’s turnaround proves successful. Shares of the FTSE 100 engine maker are up more than 1,000% in the past three years.

So, like James Bond limping out of a burning building, might the Aston Martin share price also stage its own unlikely escape?

What’s gone wrong?

The list of challenges and problems at the luxury carmaker is very long. These include sluggish sales in China, supply chain disruptions, tariff headaches, profit warnings, and consistent losses.

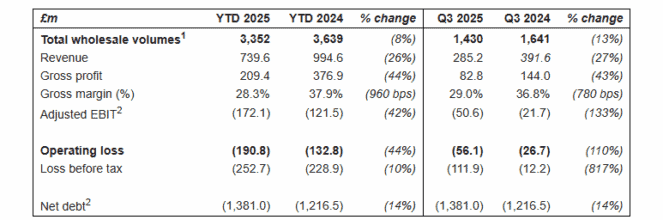

In Q3, revenue slumped 27% year on year to £285.2m, as wholesale volumes fell 13% to 1,430. Every other figure worsened, making this an alarming set of numbers to read.

One bright spot was that the first deliveries of the Valhalla hyper-car started in October. This high-margin beast could give a financial boost, assuming there aren’t any more manufacturing delays. The DBX S and Vantage S are also on the roads.

However, CEO Adrian Hallmark said the future product cycle plan is now under review. This will be done with the aim of “optimising costs and capital investment whilst continuing to deliver innovative, class-leading products to meet customer demands and regulatory requirements“.

Looking at the balance sheet, this isn’t surprising. In September, net debt stood at a whopping £1.38bn. For context, that’s more than double the company’s £595m market cap!

Earlier this month, credit rating agency Fitch downgraded Aston Martin’s debt to CCC+. That puts it deep into junk bond territory, highlighting the firm’s significant financial challenges.

Fitch said Aston Martin carries more debt and has the weakest free cash flow generation of any other carmaker it covers.

Should I take a punt on this FTSE 250 stock?

Obviously, due to the steep losses, there’s no price-to-earnings ratio. And while a price-to-sales multiple of 0.43 looks low, this doesn’t tempt me to invest. Sales are declining, dragging everything else down.

Except Ferrari, whose order book stretches into 2027, luxury carmakers are struggling. And there’s no sign things are improving yet.

Still, Executive Chairman Lawrence Stroll remains bullish, saying that his “confidence in the long-term prospects for this iconic British brand and commitment to the company remains unwavering”.

In my eyes, the most likely outcome here is that the business will be taken private (the Financial Times reported on this possibility recently). However, while this could net a tidy profit for those buying today, it might not. And I don’t invest hoping for acquisitions or takeovers.

I’ve looked at Aston Martin stock half a dozen times over the past five years. Each time, I get more bearish, and none more so than today.

Unfortunately, while I’m a big fan of the brand, cars and James Bond associations, buying the stock at 59p would feel more like a risky gamble to me.

Therefore, I think there are far safer and better options elsewhere in the UK market right now. And with 249 other mid-cap stocks to explore, there’s certainly no shortage of opportunities in the FTSE 250.