The performance of the Lloyds (LSE:LLOY) share price in 2025 was nothing short of incredible. Increasing 78% in value, the bank smashed the 20% rise recorded by the broader FTSE 100. Its gains were even more impressive considering the challenging conditions in its core UK marketplace.

What are City brokers expecting from Lloyds shares in 2026? Let’s take a look.

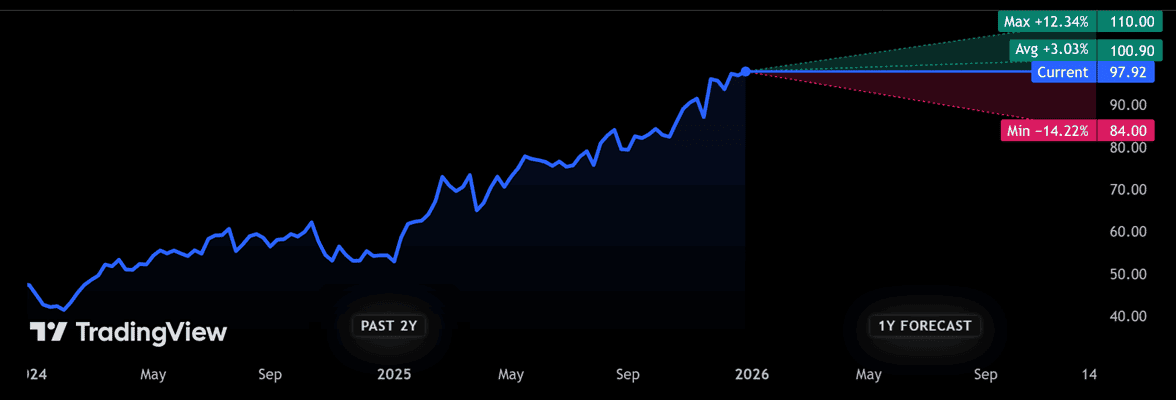

100.9p price target

The 17 analysts who cover the bank are largely confident of further price gains in the New Year. However, their average price target is just 100.9p, representing a 3% increase from today’s levels.

That’s a far cry from 2025’s spectacular gains. Even the most bullish projections are well short of the price movements recently recorded, as you can see from the chart below.

Yet brokers weren’t expecting the spectacular price performance we saw last year. Could they be wrong again in 2026?

Rock solid

Predicting near-term price movements is a famously difficult business. But if Lloyds can show the resilience it’s shown over the past year, I wouldn’t rule out further incredible gains.

So far it’s managed to navigate the challenges created by tough economic conditions and falling interest rates. Net income rose 6% in the nine months to September. Its net interest margin (NIM) was also up 10 basis points year on year at the end of the period, at 3.04%.

Leading brands like Halifax and Lloyds itself have helped the bank navigate a tough landscape, as have its leading positions in both cyclical and non-cyclical product lines. Its structural hedge, which safeguards against interest rate drops, has also helped.

A robust housing market’s another reason behind the Black Horse bank’s resilience. It’s Britain’s largest mortgage provider (market share is roughly 20%), so strong homebuyer activity has proved critical.

Importantly, 2026 is shaping up to be another solid year for the homes market. Both Savills and Rightmove expect average house price growth of 2% this year.

What might go wrong?

But can Lloyds continue to put in these robust performances? I have my doubts, with analysts expecting UK growth to slow in 2026. Rising unemployment and increasing personal and corporate insolvencies are two worrying omens moving into the New Year.

If economic conditions indeed worsen, the retail bank could see loan growth cool sharply and even reverse. It may also face a sharp rise in loan impairments (it booked £618m worth in the nine months to September).

Lloyds’ revenues and margins are also in danger as market competition intensifies. Challenger banks are rapidly expanding their operations, and raising cash to intensify their assault on the traditional operators.

Finally, it’s possible that further thumping charges for mis-selling motor finance could be coming, putting further pressure on profits. Lloyds in recent months raised provisions by a whopping £800m to cover possible costs, taking the total to just under £2bn.

What’s next for Lloyds shares?

Given these challenges, a sharp drop in Lloyds’ share price in 2026 is quite possible. In my opinion, last year’s epic price gains — combined with the bank’s current high valuation — leave the FTSE bank in danger of a sharp correction.

Its price-to-book (P/B) ratio is currently 1.5, significantly above the 10-year average of 0.9 times.

On balance, Lloyds shares might be worth considering by investors with higher risk tolerance. But I won’t be buying them for my own portfolio.