The S&P 500’s tech sector has had a bumpy start to 2026 as investors shift towards materials and energy. But the big question is whether everyone’s overreacting to the rise of artificial intelligence (AI).

A lot of investors are trying to focus on what’s happening with earnings. And while that isn’t a bad idea, they also need to think about what the numbers aren’t showing just yet.

AI in, software out

There’s a worry right now that AI’s going to disrupt software companies. But there’s been relatively little evidence of this – so far – in their earnings reports.

The rise of AI creates two main challenges for software businesses. The most basic is that their customers might switch to cheaper alternatives that offer a largely similar product.

Even if that doesn’t happen though, another potential issue is that customers won’t be willing to pay as much for software subscriptions. And that’s what makes the industry so attractive.

As a result, stocks that have historically traded at high valuation multiples are now trading more moderately. But the big question is whether or not this is an overreaction.

What disruption?

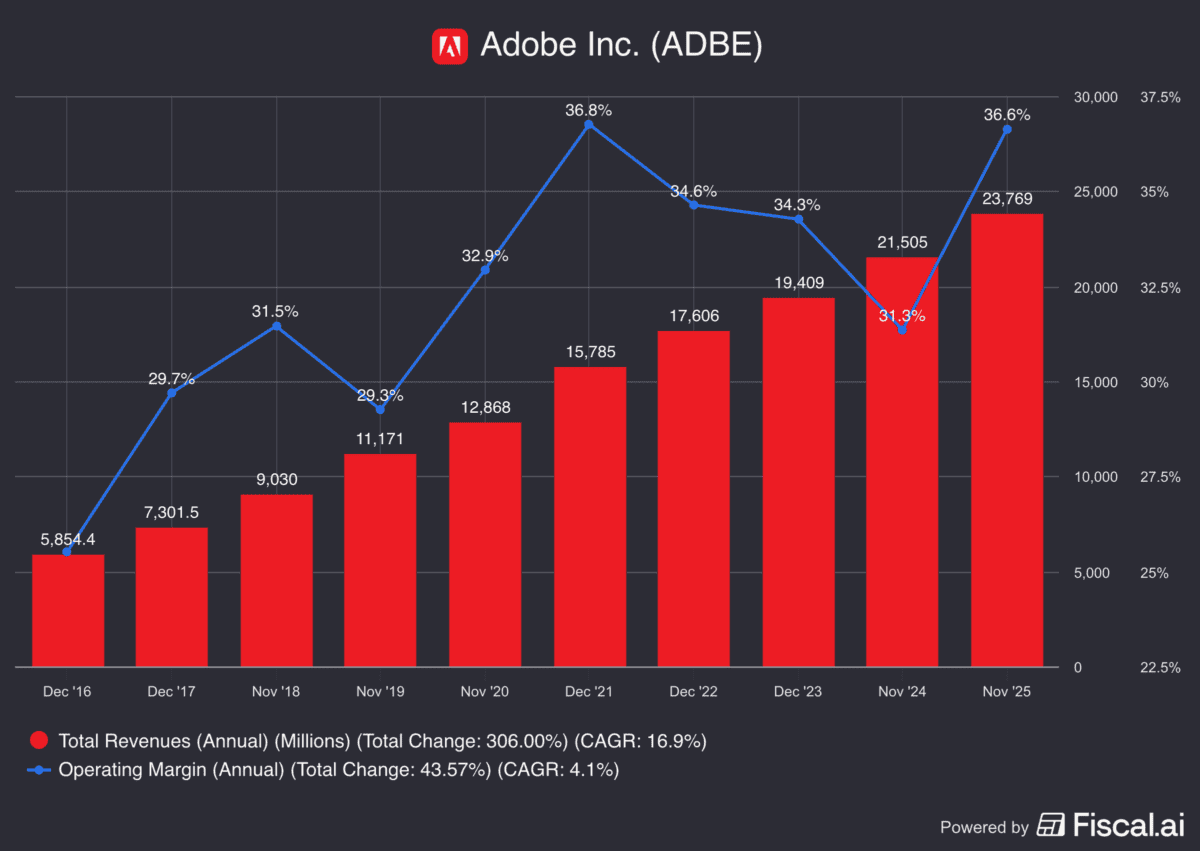

All of this sounds plausible, but bullish investors have been pointing out that there hasn’t been any sign of this happening yet. And they back themselves with charts like this one:

Source: Fiscal.ai

Adobe (NASDAQ:ADBE) shares have been hit hard by fears of AI disruption. But as we can see, revenues are growing and operating margins are still very strong.

That’s undoubtedly a very nice chart – the kind that a fund manager might be happy to show to clients. The trouble is, it doesn’t say much about the disruption risk.

One reason is that most of it is about what happened before the rise of AI – revenue growth in 2017 implies almost nothing about 2026. But there’s a much more important one as well.

Forward-looking

The stock market is naturally forward-looking. In other words, what matters to investors isn’t how much a company has been growing, but how much it’s going to grow.

With Adobe, the concern is that disruption might not show up in the next year, but when it does it could potentially be huge for the business and its profitability.

A company’s previous performance can give investors an idea about what it’s likely to do. But this is usually the case only if things are likely to be largely the way they have been.

When something major happens, looking at what a business managed to do when things were different isn’t much help. And that’s why charts like the one above are of limited use right now.

What to do?

With Adobe, the big question is whether its entrenched position with designers can allow it to keep increasing its prices. I don’t know, but the answer isn’t in charts like this one.

The risk’s hard to quantify accurately, which is why share prices are volatile. But at a price-to-earnings (P/E) ratio of 16, investors do get some compensation for taking it.

My view is that there are other software names with stronger competitive positions and those are the ones I’m buying. This is what investors need to think about – not just the numbers.