Melrose Industries (LSE: MRO) is FTSE 100 stock that doesn’t always get the attention it deserves. While Rolls-Royce has become the darling of UK investors — rightly so, given its remarkable turnaround — Melrose is a phenomenally compelling investment opportunity at a fraction of the price.

And right now, I think the market is missing it.

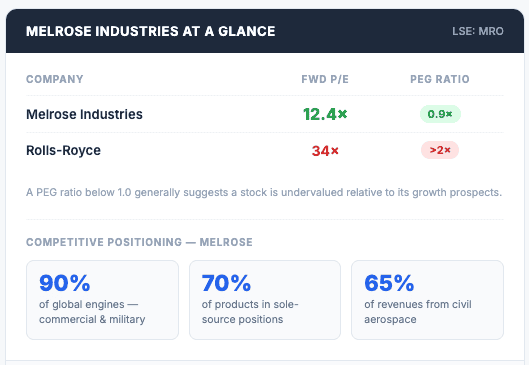

It’s rarely been cheaper

The numbers speak for themselves. Melrose currently trades at around 12.4 times forward earnings. That’s not remarkable in isolation — but pair it with a price-to-earnings-to-growth (PEG) ratio of just 0.9, and the picture changes. A PEG below one generally suggests a stock is undervalued relative to its growth prospects.

But context matters, and industry averages differ depending on things like long-term structural growth trends.

So, compare that to Rolls-Royce, which is trading at 34 times forward earnings with a PEG above two, and Melrose starts to look like a genuine bargain hiding in plain sight.

Recent weakness in the share price stems from two things: a revenue guidance miss for FY26 (lower than the market expected) and broader jitters around the conflict in Iran.

Neither, in my view, justifies the scale of the reaction — the stock was cheap even before February. Analysts agree with the average share price target sitting 41% above the current share price.

Importantly, the company recently confirmed that free cash flow has turned positive after a multi-year transformation programme.

Management called this an inflection point, and the market is already pricing in further improvements ahead. That’s a meaningful milestone for a business rebuilt from the ground up.

This is what a quality stock is all about

If you’re not familiar with Melrose, it designs, manufactures, and maintains components for aircraft engines and airframes.

The engine of Melrose’s long-term case is civil aerospace, which accounts for around 65% of revenues. The rest is military.

But the business model isn’t just about selling components, the company holds long-term engine partnership agreements that lock in recurring aftermarket revenue each time an engine goes in for overhaul.

For me, civil aviation is a strong long-term growth market with the global middle class growing steadily, compounding trends such as the inelasticity of demand for leisure travel.

Defence adds another angle. Airframe revenues in that segment rose 15% in 2025, riding a structural uplift in global defence budgets that shows few signs of easing.

Across both commercial and military markets, Melrose has exposure to roughly 90% of engines globally. Most importantly, it holds sole-source positions on around 70% of its products. That’s a real sign of quality and a competitive moat that translates into genuine pricing power over the long run.

Like everything, however, there are risks worth watching. A prolonged conflict in the Middle East coupled with higher oil prices will likely mean fewer planes in the air and lower overhaul requirements in the near term. For all involved, let’s hope that it comes to a conclusion soon.

The bottom line

At current prices, Melrose looks like one of the more attractively valued growth stocks in the FTSE 100.

A low PEG ratio, a cash flow inflection, and long-duration structural support make for a very compelling combination. I absolutely believe investors should consider this stock.