Right now, there’s an S&P 500 stock that analysts think can climb 85% from its current level. And the underlying business looks terrific.

It’s virtually a monopoly and might be harder to disrupt than investors think. But there’s a big reason I’m not buying it right now.

The business

The stock’s Fair Isaac Corporation (NYSE:FICO). It’s the company behind what people in US TV shows refer to as their FICO score.

FICO scores are essentially a way of evaluating creditworthiness. Lenders use them to work out what loans to make.

These are pretty ubiquitous. When a credit bureau like Experian checks on someone, it runs its own data through FICO’s algorithm. Importantly, the company doesn’t own customer data. Its algorithm calculates a score based on the inputs from the credit bureau.

Historically, FICO’s made money by licensing its product to the major credit bureaus. This has been a nice business for shareholders.

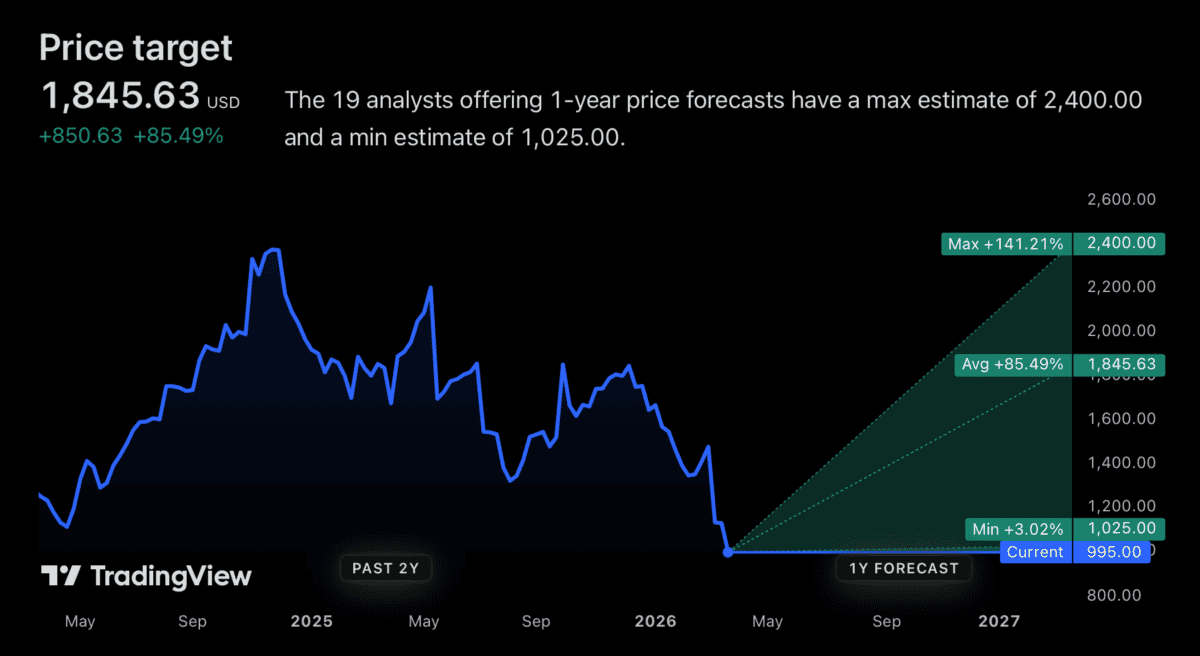

The stock however, has fallen around 58% from its highs. And whenever this happens, investors need to think why?

So why’s the stock down?

FICO’s under attack from all sides. One issue is that it’s the subject of a potential antitrust investigation. The issue is that the company unfairly uses its strength to increase prices for credit scores. And that makes for a complicated situation.

Another concern – bizarrely – is that its position is under threat. Experian, Equifax, and TransUnion are launching their own products.

FICO hasn’t necessarily helped itself here. Its attempt to disintermediate credit bureaus and sell directly to lenders might have accelerated this.

There’s also an AI threat. If artificial intelligence makes it easier to create rival products, FICO’s pricing power might evaporate. That’s why the stock’s down. But analysts seem to think that rumours of this company’s demise are greatly exaggerated.

Oversold?

FICO’s certainly under pressure. But investors shouldn’t think disrupting this business will be straightforward. Getting a credit score costs a lender around $150 for a mortgage, $5 for a car loan, and $2 for a credit card. Compared to the cost of a default, that isn’t a lot.

That means banks will have to consider whether the savings via a cheaper product are really worth it. And they might not be.

With mortgages in particular, lenders often want to resell the loans they originate. But this might be harder without a FICO score. Cheaper alternatives might be coming, but price isn’t the only issue. And that’s what the stock market might be underestimating.

UK investors

The average analyst price target is 85% above the stock’s current level. That’s the highest of any S&P 500 company.

Source: TradingView

It could be a huge opportunity. But there’s one reason I’m not buying it in my own portfolio. Share prices elsewhere have been falling and I can see more obvious stocks to buy right now. That’s all it comes down to.

Assessing the risks with FICO accurately is tricky for a UK investor like me. And I think it’s important to be honest with myself about that.

The stock might be worth considering in a market where opportunities are scarce. But that’s not the situation right now. As a result, I’m sticking to where I can see the best value. That’s what I think the best investors have always done.