A Self-Invested Personal Pension (SIPP) might be the most underappreciated wealth-building tool available to UK investors.

One of the main features is the tax relief. Basic rate taxpayers receive 20% relief automatically, meaning an £800 contribution arrives in your pension as £1,000.

Higher-rate taxpayers can claim back a further 20% through self-assessment, making that same £1,000 contribution cost just £600 out of pocket. That’s essentially free money, before a single investment decision is made.

Let’s take a look at just how valuable an SIPP can be.

Running some maths

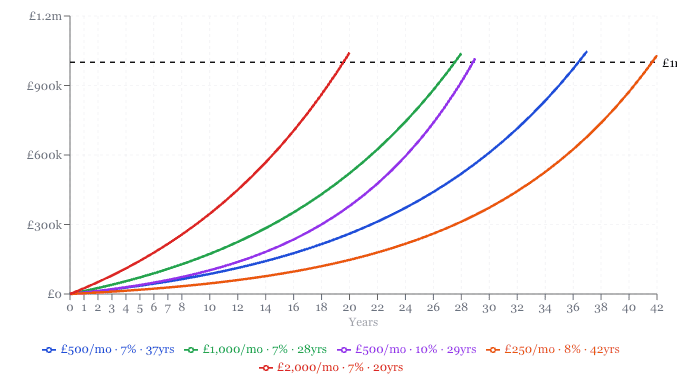

The figures below show the total landing in the SIPP — including that top-up — with growth compounding monthly. Five very different routes to the same destination:

1. Start young: £500 a month at 7% annual growth: you hit £1m in 37 years. Not glamorous, but completely achievable for a 25-year-old.

2. Double the contribution and save a decade: £1,000 a month at 7%: £1m in 28 years. Higher outlay, but nine fewer years invested.

3. Invest better: back to £500 a month — but at 10% annual growth, you get there in 29 years. Eight years faster than scenario one. Returns matter enormously.

4. The longer game: just £250 a month at 8% for 42 years produces £1,030,000. Time is doing almost all the heavy lifting here.

5. High contributions and sprint finish £2,000 a month at 7% reaches £1m in just 20 years. The most expensive monthly commitment — but the shortest horizon.

These are just a handful of realistic outcomes. However, better investors can achieve stronger returns. What’s more, you can start even earlier. We opened a SIPP for my daughter at birth. It has decades to compound before it can be accessed.

The obvious caveat: none of this is guaranteed. Investors need to make wise decisions. That could mean choosing the right index to track or buying a successful diversified fund. Or it might mean building a portfolio of high-potential stocks and shares.

Where to invest?

Like I said, knowing where to invest can be the hard part. Poor investments often lose money.

One popular investment is the Scottish Mortgage Investment Trust (LSE:SMT). The share price changes on a daily basis and reflects the value of the companies it owns.

Scottish Mortgage — a Baillie Gifford-run investment trust holding a mix of high-growth public and private companies — currently trades at a discount to its net asset value (NAV).

That gap is interesting in itself, but the stock could push higher this year and in the years beyond.

My thesis is quite simple. SpaceX makes up around 15%-16% of the entire portfolio — the largest holdings. But that’s based on December’s SpaceX valuation of $800bn. Elon Musk wants to take it public at $1.75trn — more than double. If that IPO goes ahead near that price, the maths suggest NAV could jump massively. And that’s just from one holding.

More broadly, it has a great record of picking the next big winners. Of course, nothing is guaranteed. Scottish Mortgage uses gearing — borrowed money — which amplifies losses just as readily as gains.

However, it’s something worth considering for SIPP and ISA investors alike.