The FTSE SmallCap Index has plunged in recent weeks, along with the rest of the UK market. And even though it steadied earlier this week on hopes the Iran conflict will soon end, the index is still down almost 10% since the end of February.

In situations like this, there will inevitably be wheat getting thrown out with the chaff. Canaccord Genuity seems to think so, because on 27 March the broker gave Hostelworld Group (LSE:HSW) a Buy rating, with a new 205p price target.

As I write, this small-cap is 100p, suggesting it could surge 105% over the next 12 months. While such targets are not predictions, and stocks can ultimately go anywhere, it does show that Canaccord Genuity believes the market is significantly undervaluing the business.

Why might that be? Let’s take a closer look at the stock, which is currently trading close to a 52-week low.

Niche booking platform

As a quick reminder, Hostelworld’s a travel booking site that’s particularly popular among younger and solo travellers. It has hostel and budget hotel partners in more than 180 countries, generating 7m net bookings last year.

With a £124m market-cap, Hostelworld’s still quite a small company, and it took a beating during the pandemic when much of the global travel industry effectively shut down. Another disruptive incident like this is a key risk.

However, since the end of the pandemic, business has bounced back. Last year, revenue was €93.8m, higher than before the outbreak, and adjusted EBITDA was €19.9m.

Meanwhile, the firm ended 2025 with net debt of €1.6m, a significant improvement from €13.4m in 2022. So the balance sheet is much stronger now, supporting the reinstatement of a progressive dividend for the first time since 2019.

Indeed, after falling 20% year to date, the stock’s offering a 3.4% forward dividend yield. This rises to 4.5% for 2027, based on the latest forecast.

Social travel pivot

To distinguish itself from other travel booking apps and deepen its moat, Hostelworld is developing a social network. When someone books, they get access to group chats with people staying in the same hostel, as well as link-up events (jungle trek, pub crawl, etc).

It now has over 3.4m social members, with 16m chat messages sent between them. Importantly, this social feature helps alleviate the biggest fear among solo travellers: being lonely.

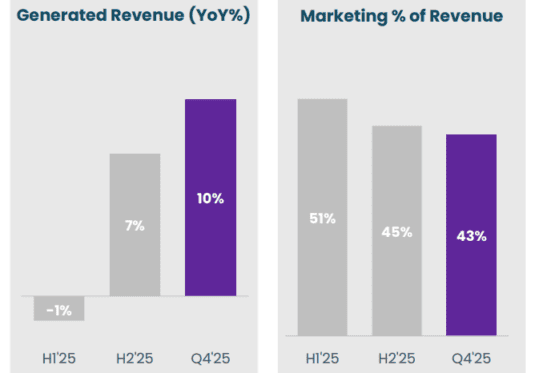

And the crucial thing here for investors is that social members are booking around twice as frequently as non-members. In other words, they’re much more likely to open the Hostelworld app next time they travel instead of searching on Google.

Consequently, marketing cost as a percentage of revenue fell to 45% in H2, down from 48% the year before. If this social network effect reaches a big enough scale, it should make Hostelworld more profitable, as well as keep travellers loyal to the app.

In November, it opened up the social platform to travellers who don’t book accommodation, adding subscription-type revenue to the mix.

Inexpensive small-cap

The stock looks cheap, trading at just 7.9 times forward earnings. Granted, this isn’t a high-growth share, but that looks decent value, especially when paired with the 3%-4% dividend yield.

Anywhere around 100p, I think Hostelworld’s worth digging into as a cheap recovery play.