City analysts see a lot of value in Hostelworld (LSE:HSW) stock right now. In fact, just yesterday (13 April), Berenberg Bank gave it a Buy rating and a 171p price target.

This is actually slightly lower than the average broker 12-month target of 181p. Comparing this to the current price of 101p, we see a 79% difference.

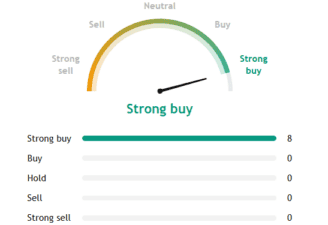

Interestingly, all eight analysts covering the stock are overwhelmingly bullish.

Of course, brokers are not always right about a stock, let alone accurate at foreseeing its near-term price trajectory. But the disconnect is striking. So what do they see in Hostelworld?

From one to three

As a reminder, Hostelworld is a small-cap stock with a market cap of £125m. It operates a platform where travellers can book to stay at over 14,700 hostels across more than 3,100 cities worldwide.

Last year, net revenue rose 2% year on year to €93.8m, with bookings growing 1% to 7m. However, adjusted profit after tax fell 14% to €15m.

Admittedly, on the surface, these numbers don’t seem particularly impressive. But whereas Hostelworld spent almost all of 2025 with just one revenue generator (hostels, obviously), this year it has three.

It now offers 18,000+ budget locations (including hotels and guesthouses) through a third-party inventory supplier. While the commission rate is lower on these, it should still drive more bookings and revenue.

And there’s Social Passes, which the company launched in November. Through these, people who haven’t booked on Hostelworld can access its social network, allowing them to message, plan trips and join events with other travellers staying in the same location.

One-time payments to access the social network range from €4.99 a week to €59.99 for the year (for digital nomads or long-term travellers). The Social Pass adds a new subscription-type revenue stream.

Additionally, Hostelworld has acquired OccasionGenius for $12m. This is a business-to-business event discovery platform that has a ton of reliable local events worldwide. Ideally, this data should inspire travellers to book trips.

Network effects

It’s this burgeoning social element where I think a lot of future shareholder value could lie. Because it’s creating a network effect, where the platform becomes more valuable as more people use it. Additional users also expand the platform’s proprietary data set.

At the end of 2025, Hostelworld’s social community reached 3.4m members. Messaging between them grew 81% year on year, with members booking approximately twice as frequently as non-members. And Social Pass members are also subsequently booking through Hostelworld.

Management said that Q1 trading had been strong, with a 3% rise in bookings expected alongside a 12% increase in revenue. So growth seems to be picking up, driven by the social travel network.

If more people book straight through the app, this should lower marketing costs and improve long-term margins.

Very cheap valuation

The biggest risk to near-term growth is the Middle East conflict, particularly inflation that might further damage discretionary spending. It could also result in higher fuel costs and therefore impact flight pricing.

However, with the stock trading at just 6.9 times next year’s forecast earnings, I think a lot of risk is already priced in. There’s also a 3.4% forward dividend yield.

Putting all this together, I reckon Hostelworld deserves further research as a deep value/recovery play.