After rising nearly 500% in a decade, Greggs‘ (LSE:GRG) shares started crashing towards the end of 2024. This coincided with new government plans to increase business tax.

Since October 2024, when Chancellor Rachel Reeves announced a hike in Employers’ National Insurance and lowered the threshold, Greggs’ shares have crashed 42%. This would have turned a £5,000 investment into £2,900, excluding dividends.

Not only did the Budget increase Greggs’ staffing costs, it arguably had a chilling effect on the UK economy. Many businesses paused hiring, pushing up unemployment, which now stands at a five-year high.

In 2023, Greggs’ total and like-for-like (LFL) sales jumped 19.6% and 13.7% respectively. In 2025, those figures were 6.8% and 2.4%, with underlying operating profit falling 4% to £188m.

Greggs under pressure

In the first nine weeks of 2026, LFL growth slowed even further, to 1.6%. And Greggs can’t seem to catch a break, with the Iran war now expected to send energy, food and fuel costs higher.

And despite the FTSE 250 company opening 121 net new stores last year, and planning a similar amount this year, investors fear we’ve reached ‘peak Greggs’. Can the brand really hit 3,000+ locations without cannibalising existing store sales? The market clearly isn’t convinced.

On top of this, the rise of GLP-1 drugs such as Mounjaro is forcing the company to adapt its menu. As a result, there are as many egg pots in the fridge in Greggs nowadays as there are sausage rolls behind the glass counter.

The growing use of GLP-1 drugs for weight loss is reshaping eating habits and reducing demand for calorie-dense foods. We research these trends and innovate with products that support satiety and balanced nutrition, including items that are high in fibre, plant-based and protein-rich.

Greggs 2025 annual report.

Is the baker at risk of losing its identity with this push towards healthier food? It’s possible.

To summarise then, there are a multitude of things weighing on the share price today:

- Slowing growth.

- Profits under pressure.

- Rising UK unemployment.

- Ongoing cost of living pressures.

- Peak Greggs concerns.

- Declining high street footfall.

- Potential GLP-1 impact.

Due to some of these factors, Greggs is currently the UK’s third most-shorted stock behind Ibstock and Wizz Air. So sophisticated investors are betting there’s more pain to come.

Not all doom and gloom

Despite the obvious challenges, Greggs still has many attractive qualities. It possesses a unique brand, strong balance sheet, and industry-leading profit margins (even after recent pressure).

Plus, there’s a well-covered forward dividend yield of 4.2%. That’s above the FTSE 250 average.

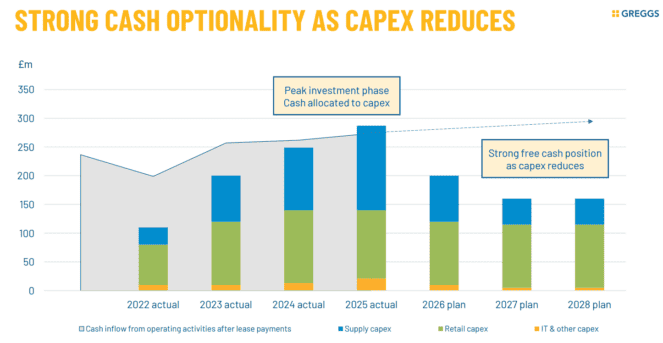

It’s also worth mentioning that capital expenditure peaked last year, which should result in significantly improved cash flow moving forward. And robotic order picking in one of its two new state-of-the-art distribution centres opening soon should improve efficiency.

Another thing I like is that around 20% of shops are now franchised (managed by third-party partners). These tend to outperform company-managed shops, as they’re primarily focused on roadside locations. And they also pick up the day-to-day running costs (rent, electricity, and so on).

Finally, the shares look cheap now. Based on forecasts for 2027, the forward-looking price-to-earnings ratio’s 12.5.

For patient investors with a multi-year investing horizon, I think the stock’s now a buying opportunity worth thinking about.