Greggs‘ (LSE:GRG) shares have fallen in a big way. But at a price-to-earnings (P/E) ratio of 13, the stock looks cheap.

A closer look though, reveals a different picture. On a free cash basis, the stock actually looks quite expensive right now.

Cash is king

A company’s cash flow statement tracks how cash moves through a business. It records how it’s generated and where it’s used. In the case of Greggs, its free cash flow for 2025 was around £74m. That’s a lot lower than the £122m it reported in net income. One reason for this is the firm had unusually high capital expenditures. These came in at £287m, which represents a big cost.

Investors however, don’t need to worry too much about this. They’re one-off investments that should be much lower in future years. There is however, something that I think they do need to pay attention to. And it isn’t reflected in the company’s free cash flow.

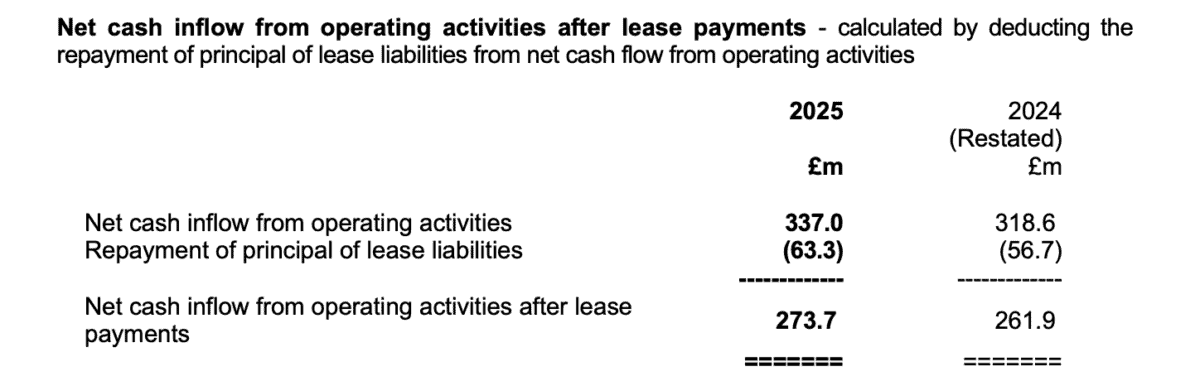

Lease liabilities

Greggs operates a lot of stores. Many of them are rented and these leases are liabilities that the company pays back each year. In 2025, Greggs spent £63m on lease liabilities. But since that’s classified as a financing cost, it doesn’t show up in free cash flow.

Source: Greggs 2025 Preliminary Results

The firm does report this clearly in its results. But it means the £288m capital expenditures exceeded its cash from operations.

I don’t expect that £63m figure to fall in future. In fact, I think it’s likely to go up if Greggs keeps opening more stores on a leasehold basis.

This is something that investors should think about. My own forecast is for around £80m in free cash flows this year and then £110m in 2027. At today’s prices, that implies a multiple of around 15. I think that’s probably reasonable, but those cash flows are still two years away.

Dividends

One good thing about Greggs is that investors do get paid to wait. The stock comes with a 4.3% dividend yield. The company didn’t increase its shareholder returns in 2025. And that shouldn’t be a big surprise from its cash flow statement.

Maintaining the dividend cost the firm a total of £70m. But that’s far more than the cash it brought in when factoring in lease payments. The firm actually took on £25m in debt during this time. From my perspective, I’d rather they cut the dividend on a temporary basis instead.

The stock market might not have liked it, but the share price has been falling anyway. And at least they wouldn’t be paying interest on the debt. Given my forecast for 2026, I’m not expecting an increase this year. After that however, things do look more manageable.

Too cheap to ignore?

Greggs’ shares look extremely cheap at first sight. But when I take a look at the firm’s leasing costs, I’m not so convinced. Based on my estimates, the stock trades at some multiples that look pretty reasonable to me. So I’m in no hurry to buy it.

There’s a lot more going on than meets the eye. And that’s without thinking about the macroeconomic outlook for the UK.