According to AJ Bell, plenty of UK investors have been selling BP (LSE:BP) shares in the last month. And it’s easy enough to see why.

Oil prices have been soaring, and investors are banking some profits on the assumption the recovery is fragile. Maybe they’re right — those oil prices have reversed on Friday (17 April). So let’s dig deeper.

Oil prices

Over the last three months, Brent crude has climbed by around 37%. And that’s pushed BP shares up 22%.

Whether or not that’s justified ultimately depends on the impact on the company’s earnings. So what are analysts saying?

Expectations for this year have more than doubled. And the impact is anticipated to continue into 2027 and 2028.

| Jan 2026 | April 2026 | |||

| Year | EPS | Present Value | EPS | Present Value |

| 2026 | £0.33 | £0.30 | £1.08 | £0.98 |

| 2027 | £0.38 | £0.31 | £0.48 | £0.40 |

| 2028 | £0.41 | £0.31 | £0.46 | £0.35 |

| 2029 | £0.42 | £0.29 | £0.42 | £0.29 |

| Total Present Value | £1.21 | £2.01 | ||

A discounted cash flow (DCF) analysis tells us what this means for the stock. A 9% target return implies an 80p per share increase.

With the stock up 103p since the start of the year, some of the selling arguably makes sense. But that’s not the only thing that matters.

Intrinsic value

Analysts might be upgrading the stock. But the boosted earnings to 2029 only account for 37% of the firm’s current share price.

In terms of enterprise value (EV) – which includes debt – the impact is smaller still. BP’s EV per share is more like £8.01.

On that basis, what matters most is what happens after 2029. An extra 80p per share in present value isn’t a huge deal.

In fact, earnings over the next few years matter less than investors might think. Even with the recent analyst upgrades.

Around 75% of the present value has to come from what happens after 2029. And that’s the thing to focus on.

Long term

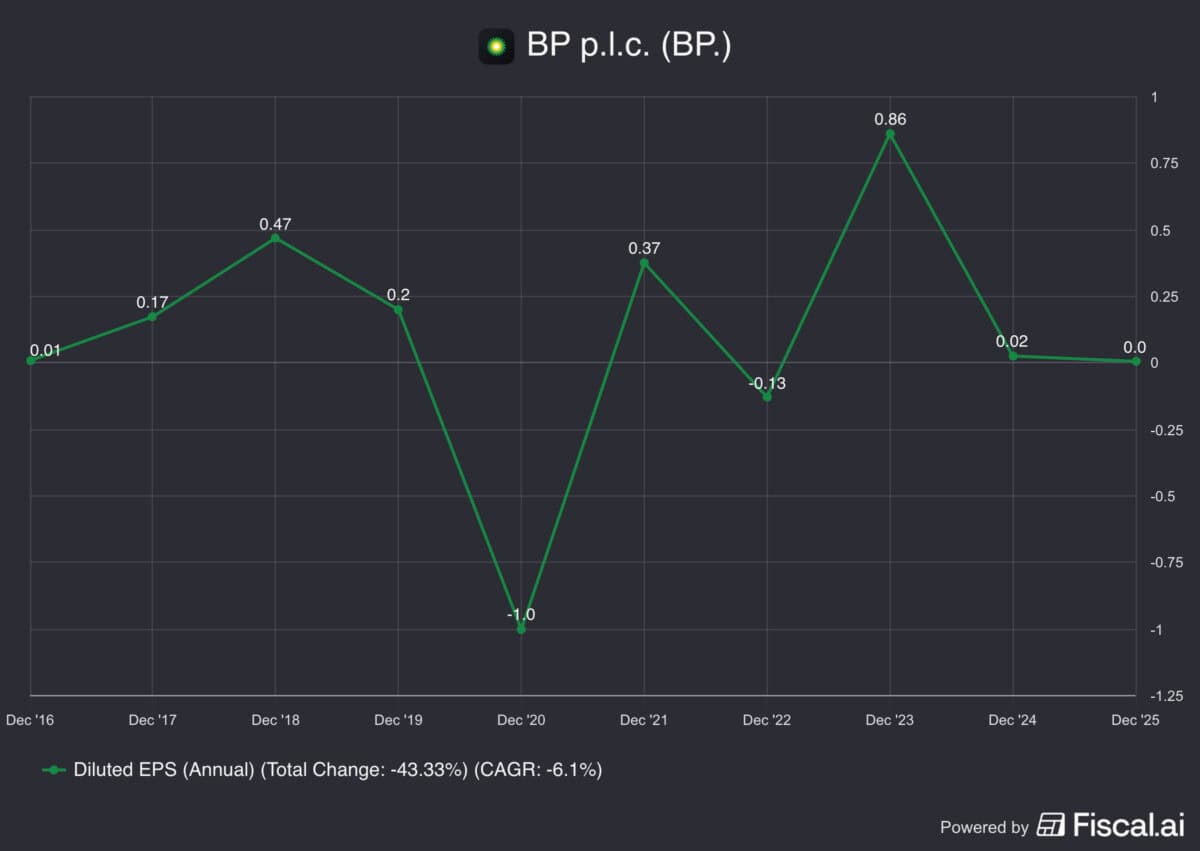

By my calculations, BP needs to average around 34p in earnings per share over time to generate a 9% return. Is that realistic?

Source: Fiscal.ai

The firm hasn’t managed this in the last 10 years. There are, however, reasons to be more optimistic going forward.

Investments in wind and solar generation have weighed on earnings. On top of this, they’ve left the firm with excess debt.

BP, however, is focusing on strengthening its balance sheet. And the windfall from volatile oil prices should help with this.

Furthermore, the new CEO is refocusing the company on oil and gas. So the same business mistakes of a few years ago are less likely to be repeated.

Time to sell?

Investors selling BP shares are clearly looking ahead. Oil prices have already started falling and that makes the stock vulnerable.

That’s a risk. But the recent volatility should give earnings a boost that impacts the firm’s intrinsic value.

My estimate of this is that it’s worth around 80p per share. On top of this, there are also lasting consequences to consider.

An improved balance sheet and a better strategic focus should help long-term profits. And these are reasons for positivity.

Investors who have owned the stock since the start of the year have done well. I’m not sure they need to think about selling yet, but I don’t see it as one to consider buying either.