I’m always on the lookout for top growth names for my ISA and Palantir (NASDAQ:PLTR) stock would certainly qualify as one of those.

That’s because, since 2020, the software company’s revenue has swelled from $1.1bn to an expected $7.2bn this year. Profits have also exploded higher, sending the share price up by an eye-popping 1,469% over this time.

Since November, however, the stock has fallen 29%. Does this represent a great opportunity to add Palantir to my ISA? Here are my thoughts.

Accelerating growth

Unlike many software companies, Palantir doesn’t operate a data platform that customers just look at. Instead, it builds software that pulls together messy, scattered data and turns it into insights that decision-makers can act on quickly in real time.

While the firm cut its teeth in the defence and intelligence world, it’s the commercial side that’s now enjoying explosive growth. Its AIP (Artificial Intelligence Platform), in particular, allows organisations to deploy large language models (LLMs) safely on their private data.

In Q4, commercial revenue skyrocketed 137% to $507m. And Palantir closed 180 deals worth at least $1m and 61 deals of $10m or more. Quarterly net profit was $609m, representing a 43% margin on total revenue of $1.4bn.

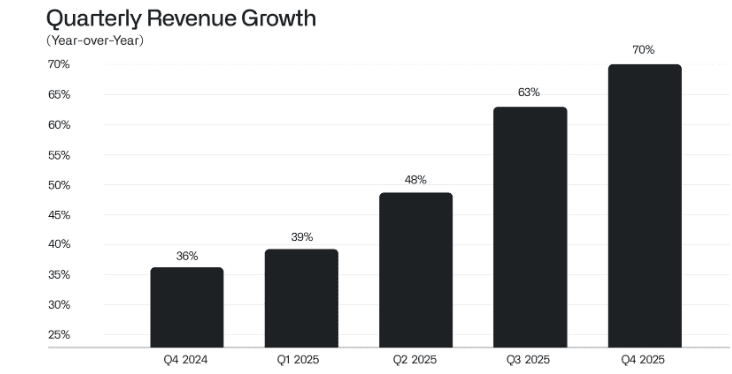

What has excited lots of investors — and sent the stock skywards — is that the company’s rate of growth has been accelerating in recent quarters.

A polarising company

Now, as impressive as this is, I do have a couple of concerns. One is that Palantir is a politically polarising company, with a bogeyman reputation among many people.

At the weekend, for example, the firm published a 22-point post online. This stated that free and democratic societies needed “hard power” in order to prevail, as well as predicting a future filled with autonomous AI weapons. Naturally, this caused a backlash in some quarters.

The question is not whether AI weapons will be built; it is who will build them and for what purpose. Our adversaries will not pause to indulge in theatrical debates about the merits of developing technologies with critical military and national security applications. They will proceed.

Palantir.

Due to rhetoric like this, some liberal MPs are calling for the government to scrap the NHS’s £330m contract with Palantir. And with its technology being widely used in the Iran war and by US Immigration and Customs Enforcement (ICE), more controversy seems certain.

The second concern relates to valuation. At present, Palantir has a massive $353bn market cap, yet is only expected to generate around $7.2bn in revenue this year. This means it trades at a forward-looking price-to-sales ratio of almost 50.

And while Wall Street analysts expect revenue to double between now and 2028, this is still an incredibly pricey stock. If growth unexpectedly slows, the valuation would almost certainly prove unsustainable.

So what’s my move?

Palantir is undoubtedly an exciting company, with super-strong margins and a long potential runway of growth ahead. The firm also has a distinctive corporate culture that keeps it innovating ahead of rivals and focused on the long term.

However, it’s also politically polarising, and I worry this may reduce its international growth prospects, especially in Europe. With the stock trading very expensively, this isn’t one I’m looking to buy for now.