Are Greggs‘ (LSE:GRG) shares undervalued? The best way to figure it out is with a discounted cash flow (DCF) calculation.

This computes an intrinsic value for a stock that investors can compare to the current price. But the output is only as accurate as its inputs…

DCF calculation

The kind of DCF calculation I’m using here needs three main inputs:

- The current free cash flows.

- A discount rate.

- The future growth rate.

The first two are straightforward enough. The current cash flows are in the firm’s accounts and the discount rate is the investor’s desired annual return.

The third input is the most difficult. A company’s future cash flows aren’t specified the way they are with a bond. That means investors have to try and figure them out. And the resulting valuation is only as accurate as the estimates they come up with.

Greggs however, is a relatively uncomplicated business. So I think investors can have a decent idea of its future prospects.

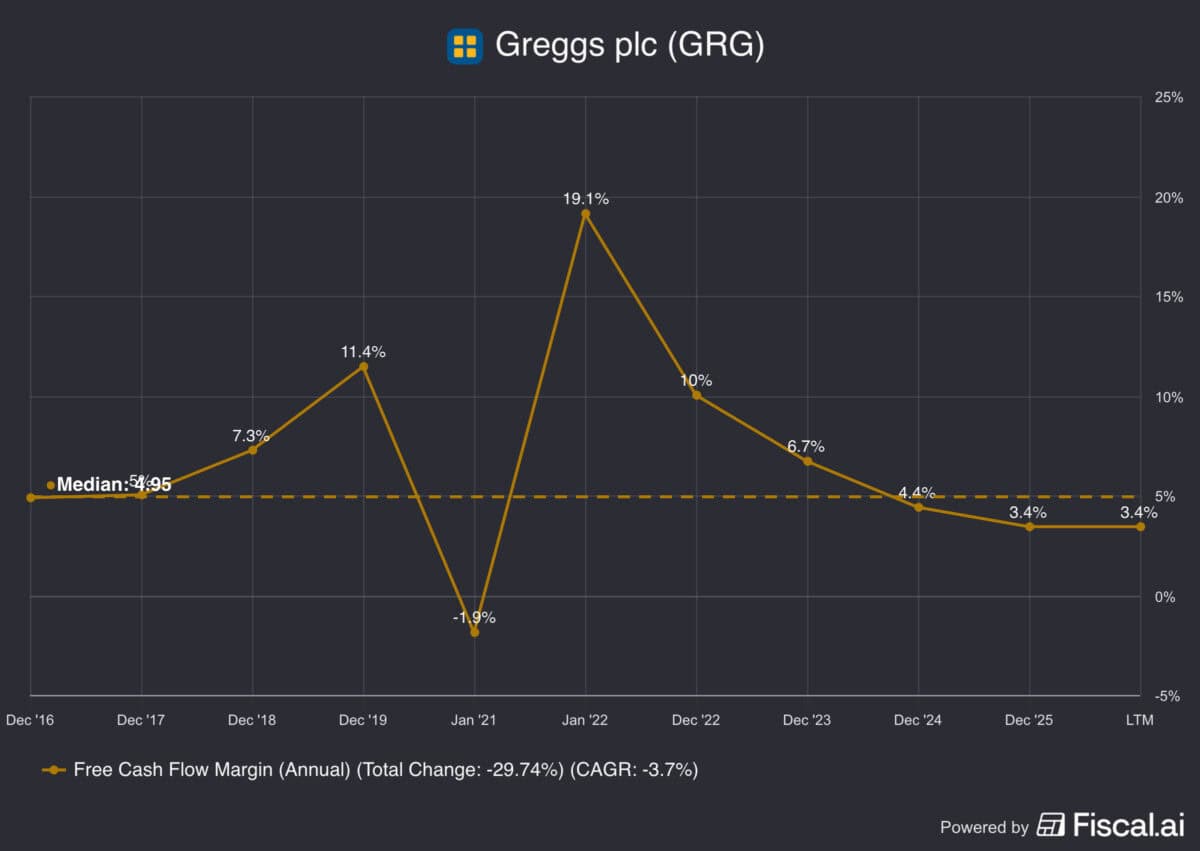

Margins

In 2025, Greggs generated £73.7m in free cash. But that was an unusual year containing some one-off investments. The company’s free cash flow margin was 3.4%. Over the last 10 years however, it’s more usually been around the 5% mark.

Source: Fiscal.ai

The difference between 3.4% and 5% might not look like much. But based on last year’s sales, it’s the difference between £73.7m and £108.4m.

There’s a lot to look at on this front. Inflation will create margin pressure, but when the firm stops opening new stores, this should improve. Given this, I think it’s worth assuming a 5% free cash flow margin in a DCF model. The next question is how much is that going to grow?

Growth

In 2025, Greggs achieved like-for-like sales growth of 2.4%. But that’s not the firm’s only source of growth going forward. In the short term, it can keep opening new stores. In recent years, this has been supporting some weak like-for-like growth figures.This can’t go on indefinitely. But when it finishes, I expect the firm to have more free cash available to support other initiatives.

One example is share buybacks. This can generate higher free cash flows per share by reducing the overall number of shares outstanding. Given this, I expect Greggs to be able to generate 5% overall growth in future. The source of that growth will change over time, but that’s my forecast.

How much is it worth?

So in looking to work out an intrinsic value for Greggs’ shares, I have the following assumptions:

- Normalised free cash flows of £108.4m (based on a 5% margin).

- A 10% discount rate (my target rate of return).

- A 5% growth rate (from a combination of higher sales and share buybacks).

Based on this, a DCF calculation generates a valuation of £2.25bn for the entire business. And that implies a share price of £22.05. With the stock at £14.67, that’s a huge 50.3% discount from the current level. So if what I’m assuming is correct, the stock’s undervalued.

It’s worth reiterating that there are no guarantees. But these are my current best estimates and I’ll look to return with future updates. If I’m right – or even close – the discount means the stock’s worth a closer look. Unless, of course, there are even better opportunities elsewhere…