A year ago, I could buy Glencore (LSE: GLEN) shares for 354p. Today, they’re trading around 12% higher, turning a £5,000 investment into roughly £5,600. There’s been a small dividend along the way too, but that’s not the point.

The point is volatility.

In April, during the tariff-driven sell-off, the shares slumped to a three-year low. Since then, they’ve surged 95%. That kind of price action isn’t unusual for a miner – but it does leave investors wondering what comes next.

So can shareholders expect another bumpy ride in 2026? To answer that, I focus on one metric that cuts through the noise.

Alternative performance measure

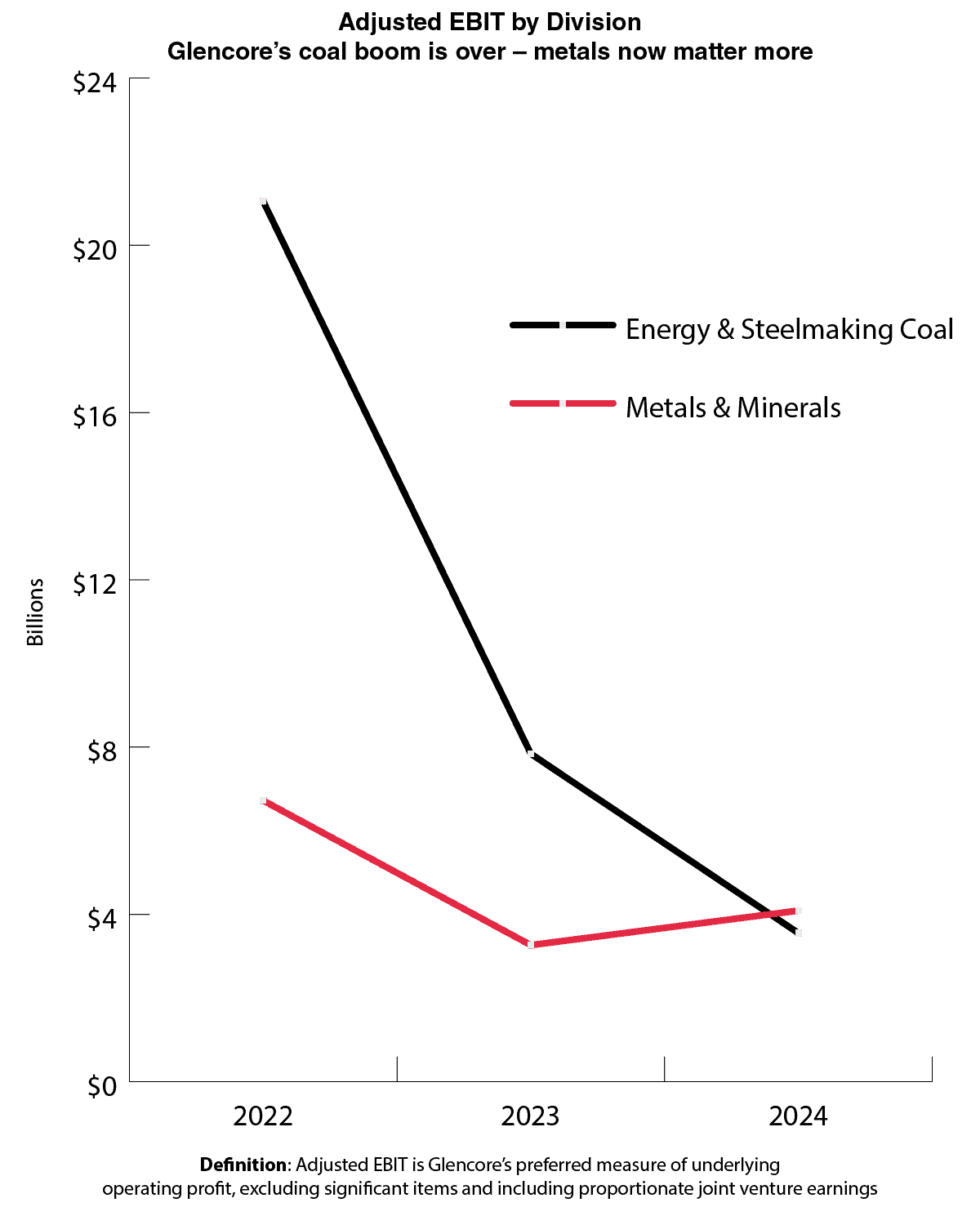

Adjusted EBIT (earnings before interest and tax) is the miner’s measure of underlying operating profit. It strips out significant items, such as one-off asset sales or impairment charges, giving a clear view of which parts of the business are actually generating profit.

The chart below shows Glencore’s adjusted EBIT over the past three years.

Chart generated by author

In 2022, energy and steelmaking coal generated an extraordinary profit windfall, dwarfing metals and minerals. That year now looks increasingly like a one-off.

Since then, coal earnings have collapsed. At its H1 results, the miner reported that Newcastle thermal coal prices had fallen by 20%, while hard coking coal prices were down by a third year on year. This comes on top of already steep declines in 2023.

That narrowing gap matters. It suggests the miner is no longer leaning on coal to prop up the income statement in the way it did during the post-Covid commodity spike.

Copper is the future

What’s most instructive about the EBIT chart is that, despite weak copper prices in 2023 and 2024, the metals division’s underlying profitability held up far better than many might expect. That resilience bodes well for full-year 2025 results.

Copper has had an excellent year so far, up 32%, with pressure building on both the supply and demand side. Demand from electrification, renewable energy, and AI infrastructure continues to rise, and there are few signs of that slowing.

On the supply side, fears that the US administration could impose new tariffs next year have prompted traders to accelerate shipments into the US, stockpiling metal there while tightening availability elsewhere.

At the same time, disruptions at major copper-producing mines in Chile and Indonesia have deepened concerns about global supply. With new discoveries thin on the ground, bringing meaningful new tonnage online won’t happen overnight.

Major risks

Copper prices remain volatile and could fall sharply in a global recession. Coal is still Glencore’s largest revenue generator, so prolonged weakness would weigh on cash flows. Geopolitical and regulatory risks are ever-present across its operating footprint, while weather disruptions and operational setbacks could also derail production targets.

Bottom line

The key takeaway from the EBIT chart is simple: metals are shaping Glencore’s future.

Only this month, the miner cut around 1,000 jobs as part of a restructuring that bets heavily on rising copper demand. The plan is to lift copper production to around 1.6m tonnes a year by 2035, positioning Glencore among the world’s largest producers. This year, output is expected to reach 850,000 tonnes.

The journey won’t be easy, but the trajectory is clear. That’s why I’ve been adding to my exposure to the miner throughout the year.