And ISA is one of those uniquely British inventions that are often viewed far too narrowly. The main point of them isn’t just how much you save, but how time turns those savings into long-term passive income – and the choices that come with it.

What time really buys

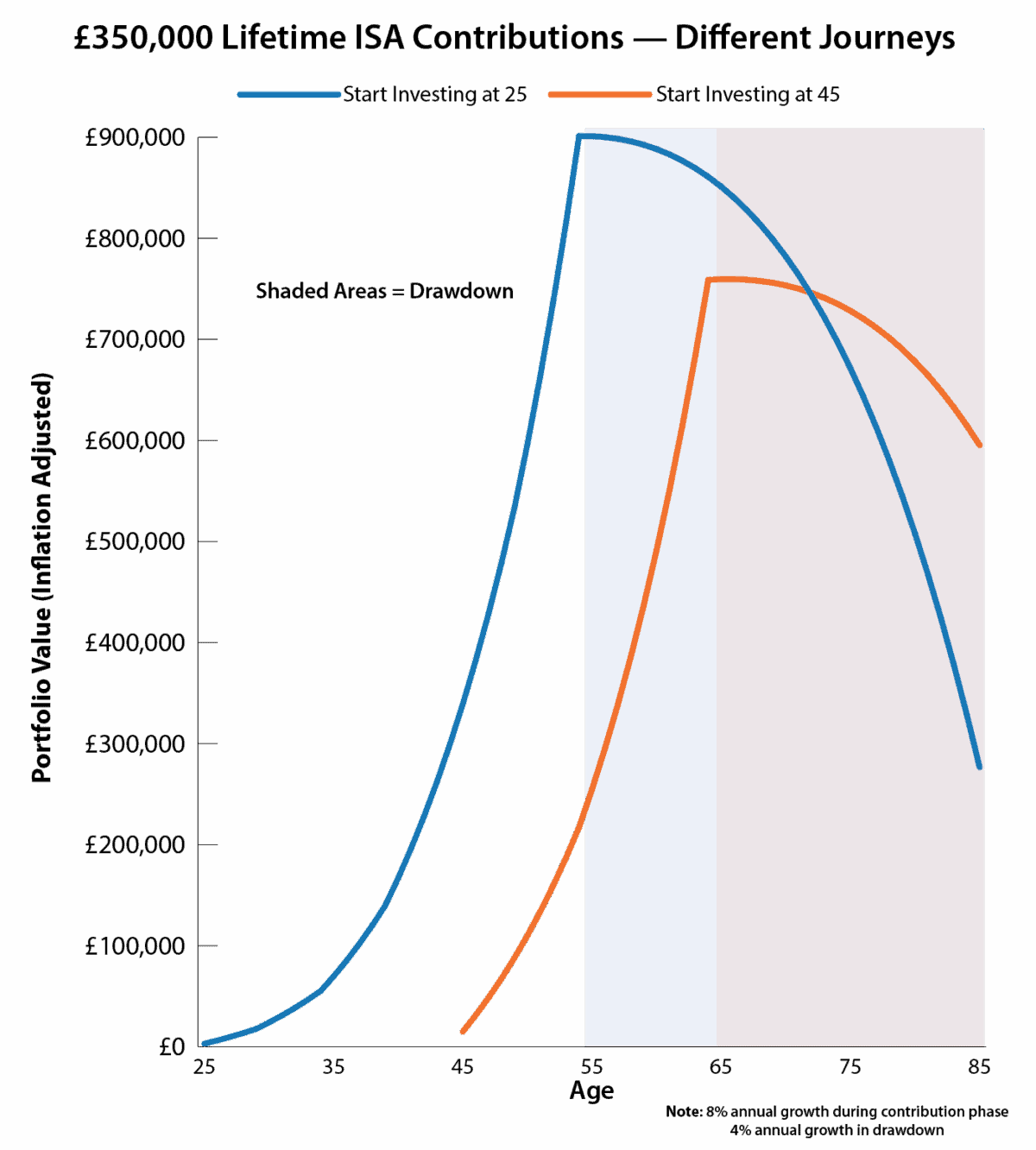

The chart tells the story better than any spreadsheet ever could. Two investors. The same total contributions. Very different starting points. One starts early and builds gradually. The other starts much later and saves hard. By retirement, the gap in portfolio size isn’t as dramatic as many might expect. But how they get there is everything.

Chart generated by author

The £20,000 income shown is inflation-adjusted. That matters. It’s why the earlier starter appears to withdraw more at the outset – prices have had decades to rise quietly in the background. The later starter begins withdrawals sooner, so the initial income looks lower in today’s terms.

Returns are also assumed to fall in retirement. Not because markets suddenly stop working, but because most people naturally reduce risk once their salary ends. Growth gives way to preservation. It’s a subtle shift, but over long retirements, it really adds up.

Optionality

Where time really earns its keep is before retirement. Starting earlier creates choices during your working life: the freedom to pause contributions, take career breaks, ride out market crashes, or simply ease off when life gets in the way.

Early contributions do most of the heavy lifting. Later ones can still be powerful – but they’re far less forgiving.

The late-starter route can absolutely work. But it demands consistency, higher savings rates, and leaves much less room for error if plans change.

This isn’t about a right or wrong approach. It’s about understanding what time actually buys you. The chart doesn’t just show growth – it shows how starting earlier turns flexibility itself into an asset.

Under the radar

Many investors assume the only way to build passive income is by owning high-yielding shares. I don’t take that view.

You see, I didn’t buy Asian insurance giant Prudential (LSE: PRU) for its headline yield – currently around 2%. Instead I bought it for the long-term compounding opportunity across underinsured Asian markets. Insurance penetration remains in the low-single-digits, while the region’s protection gap is estimated at more than $100trn. That’s a powerful backdrop for growth.

In 2025, the shares are up 75%, making them the best performer among its FTSE 100 insurance peers. Even so, I’d argue the stock still sits under the radar for many investors.

China exposure does introduce volatility, and policy risk shouldn’t be ignored. The bursting of the property bubble has clearly dented the country’s growth story. But much of that uncertainty appears to be reflected in the valuation, in my opinion.

What really appeals to me is the capital flexibility. Between 2024 and 2027, Prudential expects to return more than $5bn to shareholders, combining a 10% annual increase in the dividend with a $2bn share buyback programme.

With the Chinese government actively encouraging stock market participation, Prudential looks well placed to benefit. Strong distribution, a trusted brand, and deep expertise across Asian markets are why it earns a place in my Stocks and Shares ISA. It’s not a pure income play today – but it gives me valuable optionality for the future.