When looking for stocks to buy, the publication of a company’s annual results can often help focus the mind. These milestones are useful because not only do they provide an insight into what’s happened but, more importantly, they provide some clues as to what could happen.

This is significant because investors tend to be forward looking and share prices – in theory, at least – are supposed to reflect future cash flows.

So what are we to make of Wednesday’s (25 February) results from Rolls-Royce Holdings (LSE:RR.)? Is the group’s epic share price rally likely to run out of steam? Let’s delve a little deeper.

Better than expected

For 2025, the group comfortably exceeded expectations. It reported an underlying operating profit of £3.46bn and free cash flow of £3.27bn, beating analysts’ forecasts by 5.8% and 2.5% respectively. Over the next three years, share buybacks of £7bn-£9bn were also announced.

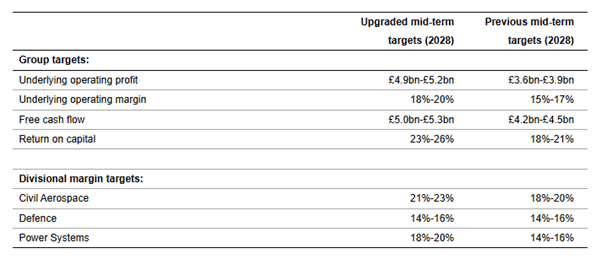

Its underlying earnings per share was 29.44p, meaning the stock’s now trading at an eye-watering 47 times historic earnings. But I think this is more palatable given that Rolls-Royce also massively upgraded its mid-term (2028) targets, including announcing a significant increase in its expected return on capital.

Looking further ahead

Beyond this forecast period, the group said it’s “well-placed” to become the market leader in small modular reactors (SMRs). By 2030, it noted the division will be “profitable and free cash flow positive”.

In addition, the group’s eyeing an “opportunity to re-enter the large and growing narrowbody [aircraft] market”. This will be done through a partnership and could be a game changer. In 2025, its civil aerospace division accounted for 61.5% of underlying operating profit (£2.13bn). Achieving a small fraction of this number could help drive the share price much higher.

Of course, it’s easy to say these things. Delivering these ambitions is much more difficult. But since the pandemic, Rolls-Royce has consistently proven the doubters wrong. I’m happy to admit that I was one of those. I was late to the party but, even so, the stock’s now the best performer in my ISA.

But there are still some challenges ahead. With such a strong valuation multiple, any sign that the group’s not on course to meet its upgraded targets is likely to lead to a sharp correction in its share price. And there are no guarantees that its SMR technology will work. The Nuclear Energy Agency has identified 127 different designs, none of which are currently commercially viable.

My verdict

However, despite the group’s generous valuation and its healthy post-pandemic recovery, I still think Rolls-Royce is a stock to consider buying. And others appear to agree with me. A few hours after publication of its results, its share price was up over 5%.

I reckon investors were impressed with the group’s performance across each of its three business units. In 2025, large engine flying hours increased by 6%. Data centres are helping drive revenues and margins higher in its power systems division. And at the end of the year, its defence arm had an order backlog equivalent to three years of revenue.

With all three powering ahead — and possibly more to come from SMRs and engines fitted to smaller aircraft — I think it’s a stock to consider buying and holding for the long term.