Large share price movements always attract my interest. It was no different on Thursday (26 March) when this FTSE 250 stock crashed 10.8% after the company announced the departure of its chief executive. And as is often the case after bad news is released to the market, I saw a particularly exciting opportunity.

Let me explain.

Something unexpected

Electrical retailer Currys (LSE:CURY) surprised investors by announcing that its boss, Alex Baldock, was to step down. It wasn’t revealed where he’s going.

Given that the group also announced that current trading was in line with expectations, the share price drop was clearly attributable to Baldock’s departure.

I don’t know Currys’ chief executive but what I’ve read about him is all positive. In particular, he’s been highly praised for batting off a hostile takeover that would have seen the group being sold for over 40% less than it’s worth now. And he’s been responsible for “transforming the business in the face of some difficult headwinds”, according to the group’s chair.

On this basis, I think he can justify the £3.82m pay package he was awarded for the 53 weeks ended 3 May 2025 (FY25).

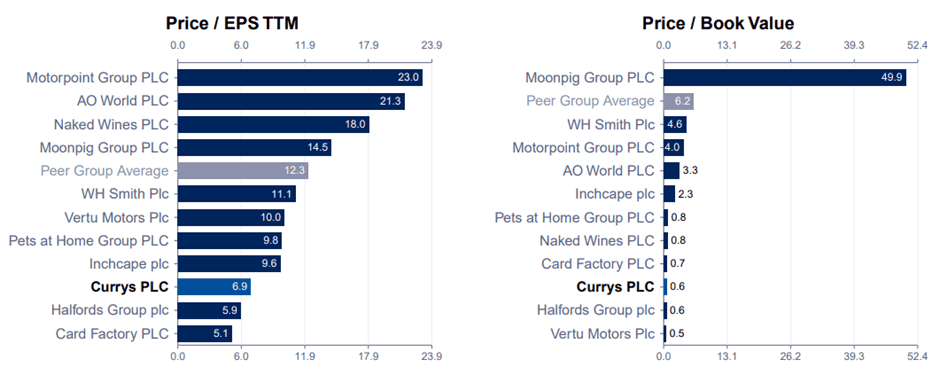

However, as much as I rate him, I don’t believe his departure can justify wiping £148m off Currys’ stock market valuation. If he was a listed business, he’d have a price-to-earnings ratio of 38.7! That’s more than Nvidia’s.

For comparison, the electrical group’s five-year average (median) is 6.9. By coincidence, this is the level at which the stock currently changes hands. And compared to others in the sector it’s on the low side.

The group’s balance sheet also suggests that its shares offer good value. It has a price-to-book ratio of only 0.6.

All eyes on summer

With 2026 a football World Cup year, the group could experience a summer bonanza. Big tournaments usually lead to increased TV sales.

For example in 2014, Tesco reported that television sales had doubled ahead of the World Cup kicking off in Brazil. In 2018, John Lewis saw a 140% rise in the sale of big-screen TVs on the day of the opening ceremony compared to the same day a year earlier. And in 2022, OnBuy reported a 1,769% spike in demand for home cinema systems before the first game in Qatar.

It’s estimated that Currys has a 30% share of the UK TV market. It’s probably something similar in the Nordic countries in which it operates. And with 393 different models listed on its website, there’s plenty of choice for football fans looking to upgrade.

In light of these factors, I thought the investor over-reaction was a good opportunity to buy a few shares in a business that retains a strong brand, healthy balance sheet (it has a net cash position) and one that’s expecting a 11%-17% year-on-year increase in its adjusted profit before tax when it reports its FY26 results.

Of course, the group’s likely to suffer if there’s another economic slowdown. And its margin could be squeezed if supply chain inflation starts to pick up once more. However, the group’s successfully navigated bigger challenges before.

Personally, I reckon it’s one of many undervalued UK stocks that could be considered by investors on the lookout for a bargain.