The Helium One Global (LSE:HE1) share price was on a strong rally until, at the end of March, the gas explorer announced it needed to raise some more cash. At the start of the year, the group’s shares were changing hands for 0.46p. Just before news of the fundraising was released, they were fetching 58.7% more (0.73p). Now (2 April), they’re trading around 0.6p.

But repeatedly asking shareholders for more money is inevitable if a company isn’t generating any revenue. How else can it pay the bills? Risk-averse banks are generally reluctant to lend in these circumstances. However, things could soon change.

Good news

The group has a 50% interest in the Galactica-Pegasus project in Colorado, which is about to become fully operational. Here, the price for the first helium has been agreed and the project’s transitioning to a 24/7 operation. Carbon dioxide sales will soon follow.

As distasteful as this might sound, reaching this milestone has been perfectly timed. The bombing of the Ras Laffan gas facility in Qatar — and transport disruption following the effective closure of the Strait of Hormuz — have driven helium prices higher.

Taking advantage

To capitalise on progress in America, new cash of £5m has been raised from a share offer to institutional and private investors. The retail offer was over-subscribed so the company decided to take the opportunity to raise £500,000 more than was originally planned. However, disappointingly for existing shareholders, the shares were issued at a 17.6% discount to the prevailing market price.

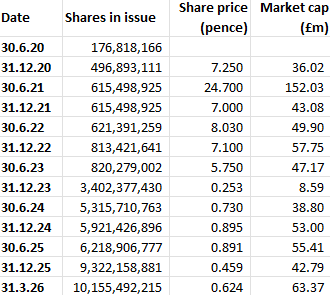

In some respects, the directors can pat themselves on the back for getting this far. Gas exploration is time-consuming, technically challenging, and expensive. Yet, since the group’s IPO in December 2020, its market-cap’s risen by around £43m.

However, it’s come at a cost to shareholders who haven’t participated in the numerous fundraising rounds that have seen the group issue nearly 10bn more shares. Someone who invested £1,000 at the time of listing would now see their stake valued at just over £200.

Thousands of miles away

But Galactica-Pegasus is relatively small. A much bigger opportunity lies deep underground in Tanzania. To transform the company’s value, it has to demonstrate that it’s able to extract the helium from water aquifers, transport it cheaply off the African continent, and find some customers.

The latter shouldn’t be too difficult given the unique cooling properties of the gas. Even before the conflict started in the Gulf, there was a worldwide shortage, which kept prices at historically high levels.

And If the group’s able to overcome these challenges, the value of the group could soar. Panmure Liberum has set a price target of 3.6p for the group’s stock. The broker says the “world-class discovery” in Tanzania, along with what’s happening in the US, means the stock’s significantly undervalued.

Next steps

But the trouble is it’s going to cost a lot of money to commercialise the Southern Rukwa project in Africa. Initial estimates have been put at $100m. However, nobody really knows for sure. The company’s seeking a strategic partner to help share the burden but, in my opinion, further dilution for shareholders looks certain.

That’s why the stock’s too risky for me. On balance, I think there’s a better chance of making decent money from a miner already producing.